100 Money Saving Tips

Here are 100 money saving tips you can use to pay off your debt, give or save to invest. If you like it please share on your favorite social network.

- Adjust the Thermostat In the summer turn it up and in the winter turn it down. You will use less energy. Get a programmable thermostat if your house is empty during the day; you can save a lot of money and still have the temperature you want in your house before you get home.

By Jess from Canada (HPIM4771) [CC-BY-SA-2.0], via Wikimedia Commons

- Cut the cable Cable TV is becoming increasingly expensive as well as increasingly redundant since most networks are putting their content online, either on their own websites or on sites like HULU.

- Combine it if you can’t cut the cord then at least find out if you can bundle the services and save money in the process.

- Threaten to cancel and see what kind of deal you can get; Cable companies are striving for subscriber numbers right now and just want to hold onto their current clients. You can get a greatly reduced rate if you just tell them you want to cancel.

- Entertain at home A game night or a nice dinner is much cheaper and nicer in many cases, when done at home. Find other like-minded people and find creative activities.

- Learn how to sew a button Don’t throw away clothes because of minor issues. Sew the button back on if you stain your jeans or rip them make them your yard work jeans.

- Make gifts don’t buy them Making quality gifts takes time, but the person getting the gift may appreciate it much more.

- Convert to a gas or an instant water heater They are more efficient and can save a lot of money over time.

- Replace incandescent bulbs with CFL although there is some debate on this you can test and see if it helps you save money.

- Get rid of your home phone With cell phones being what they are now there is very little reason to have a land line. If you don’t get the best service at your home many cell phone providers will give you a device that will boost the signal in your home. It is like having a tower in your house.

- Shut vents in unused rooms This may not be a good idea if you have forced air heating, but shutting vents in unused rooms can save on your heating and cooling bill.

- Change the filters in your home every 6 months This makes your HVAC work more efficiently

- Use a power strip to turn off your entertainment system There is a term being used call vampire power where a lot of new electronics draw small amounts of power even when they are turned off. Using a power strip can eliminate that power draw and save you money.

- Buy used when possible Pay extra for a used quality product instead of a disposable quality product. Especially when it comes to kids items that they will outgrow in 6 months.

- Get live in help If you have a spare room you can rent it out to someone you trust.

- Pay your mortgage on a bi-weekly schedule Doing this can shave years and thousands of dollars from your mortgage.

- Clean your own carpets You can rent the machine or borrow it from someone.

- Attend College online It is much cheaper to get your education online just do your research and find a good school. I just finished my degree in 2.5 years.

- Delay purchases When you have a desire to purchase something wait a few days maybe even 30 to make sure you still want to spend the money on it.

- Buy a Clothes line Running a dryer costs a lot of money. This can be your first wind and solar power appliance.

- Create your own 100-calorie snacks Buy in bulk and divide it yourself. That packaging costs a lot and we pay for it in the end.

- Make drinks at home If you are going to have alcohol it is much cheaper do have drinks at home with friends than to do it at a bar.

- Clean dryer filters It helps you dryer work more efficiently and prevents fires.

- Clean refrigerator coils again it improve the efficiency of your fridge.

- Turn down the temperature on your water heater It can save a lot of money on energy. Unless you are like me and LOVE your HOT showers.

- Start a garden If you have any space it is a great rewarding experience. It takes some practice but you can grow your own food and it will be much better for you if you are doing it yourself.

- Start a compost pile Take your yard waste and kitchen scraps and start a compost pile or a worm bin and make your own Black Gold

- Reuse milk jugs You can use milk jugs with small holes in the bottom as a drip irrigation system.

- Don’t waste your water When you cook veggies with water, steam or boil. Use it to water your potted plants. The nutrients lost in the water will feed your plants. Just remember to let the water cool before you use it or it will kill your plants.

- Make your own cleaners Vinegar has tons of uses around the house and you can mix some up to clean and deodorize your home.

- Try a staycation If you stay home but disconnect from your normal routine you can get things done around the house or in your local area and save a lot of money.

- When possible go for energy saving appliances Save money in the long run with better energy ratings.

- Wear clothes more than once before washing when possible Unless if you are getting really dirty or are working really hard you can get away with more than one wear.

- Buy your own water filter Bottle your own water.

- Eat early or late when going out You can get early bird discounts or happy hours to save money.

- Keep your freezer full It takes more energy to keep an empty freezer cold.

{kind=link}

Kids

- Create a Babysitting Co-Op No not like those books from such a long time ago but if you and another couple can exchange babysitting services it will give both of you a free night out. This is great for your marriage as well as your wallet.

- Hand me arounds There is no reason to buy all new clothes for your child, especially when they can only where the same thing for a few months before they grow out of it. When you are done pass them along and find someone else to do the same with. My wife has a Mothers group at church that constantly passes clothes around and saves everyone a ton.

- Play at the Public Park Why not just go to the park and play with other kids, you already paid for it.

- Watch the local parks for educational programs Take your kids to these and they may have so much fun they won’t even realize they are learning.

- Public Libraries There is so much that can be had at public libraries from internet access to the books and learning programs.

- Use city services There are plenty of free (already paid for through taxes) activities for children around our city, between Metro parks and libraries there is plenty to keep them entertained.

- Watch local churches Especially in the summer there are tons of Vacations Bible Schools for kids’ activities.

- Stop spending so much on your kids Really they want your time and love more than anything. Make up games you can play at home all the time or just play tag.

Car

- Slow Down Aggressive driving and decrease your fuel efficiency by up to 33% according to the EPA.

- Driving the speed limit This also helps to save gas as gas mileage drops over 60 MPH.

- Empty your Trunk Getting excess weight out of your vehicle will give you better gas mileage.

- Change your oil Keep up with routine maintenance these jobs are not just to keep auto shops in business but they help your car drive better longer.

- Never buy new New cars are almost always a bad deal because of depreciation. Used cars will get you a much better bang for your buck

- Wash and vacuum your car at home There is no reason to pay for a vacuum and the automatic car washes don’t do the best job of your car.

- Wash it often Dirt can damage paint.

- Keep your tires inflated It will help you get better gas mileage; you also need to check them every few weeks.

- Use 2WD55 Air conditioning That is two windows down 55 MPH.

- Keep wheels aligned Your car is working hard if your alignment is off.

- Rotate your tires Prevent wear and make your tires last longer

- Find a way to carpool if possible I was able to carpool for over a year with a friend over a 40-minute commute, so it saved a lot of money.

- Leave the car behind Walk whenever possible, ride your bike if it is too far to walk.

- Move to just one car Can you do with only one car in your family, save on insurance, gas and maintenance?

- Look for discounts Ask your insurance company if you can get a discount for paying annually or with an automatic draft from your checking account.

Electronics

- Shop around. There are so many places to get a good deal online that you have to do your research.

- Buy Video games with replay value I have never been more disappointed than with THE video game that was supposed to be the be all end all of games and it took me 12 hours to finish. Some games you can play for hours some for days. Do the math 5/hr or .10/hr?

- Get books and DVDs from the Library Most libraries are stocked with DVD and unless it is a reference book you will need constantly you can get it for free at the library. If the library doesn’t have it, try sites like www.paperbackswap.com and www.dvdswap.com OR Find a friend who has it and borrow it. If you still can’t find it shop the used book stored then used on Amazon.com Then the retail store if you must.

- Think about an old fashioned solution? If people like Nelson Rockefeller can run multi-national corporations without a smart phone maybe we can too.

- Look into open source software Why pay for software when there are free and sometimes better solutions out there. http://www.osalt.com/ is a site dedicated to finding you the open source solutions you need.

- Check out Ting – Ting runs on the sprint network, if you don’t mind having an older phone for a while you can save a ton of money by switchting over to ting.

Banking

- Find the best interest rates around don’t just use the bank you always have. This isn’t 1950; banks don’t think of you as anything but a number (unless you have a very special bank) so don’t fall for their loyalty stuff. If they aren’t making the most of your money someone else will.

- Call your credit cards and ask for a better rate Although I had one bank drastically reduce my limit when I did this once when all the banks were tightening up. I paid off the card and haven’t done business with them since.

- Always use a reward Card. There are not as many as their used to be but they are still out there. Get paid if you can as long as you pay off the balance.

- Get an online savings account They tend to have higher interest rates than brick and mortar banks. I use and love Capital one 360

- Don’t overdraft your account it costs you too much money.

- Pay bills automatically Use bill pay from your bank to avoid late fees and save on postage.

- Keep your money in hard to reach places like an account you don’t have Internet access to. That way you are less inclined to spend it on a whim

- Freeze your credit cards Literally we have kept our cards in a tin can full of water in our freezer. If we need them we have them but we can’t just get them to spend carelessly. Especially when you can’t microwave it.

Shopping

- Sign up for rewards Programs I even set up a special email for them but you can get some good coupons and deals from a lot of these.

- Stick to the list A shopping list is not just there to remind you of what you need to buy but, it is also there to prevent you from buying things you don’t need.

- Drink more water Soft drinks at a restaurant can cost up to $3. If you drink water you will save a lot in the long run. Even at home it is cheaper.

- Buy more ingredients Prepares, processed, microwave meals are more expensive and less nutritious than buying the ingredients and making it yourself. We have seriously considered a “you can anything you want as long as you make it yourself rule)

- Buy and cook in bulk Wholesale clubs allow you to buy large amounts at a discount (although not always so keep an eye out). Store the food for later or prepare it all at once and then freeze it for use later.

- Constantly shop around on service like insurance Insurance policy rules are constantly changing you may be able to get a better rate from someone else check at least once a year.

- Check your deductibles you can save a great deal by increasing your deductibles, although make sure you have the money to cover your deductible in the event of an accident.

- Always ask for a discount The worst thing they can say is say “No” and it is easier every time you ask.

- Don’t be trendy Classic clothes last longer than trends. Besides you will most likely look back and realize how silly you looked

- Don’t buy dry clean only clothes You don’t want to spend the extra money

- Shop at outlets and stores like TJ Maxx “ You can often find better prices at these stores.

- Share a Meal If you are going to go out to eat try splitting a meal. Most casual dining restaurant meals are big enough to share and still be full.

- Buy a whole Chicken You can eat all of the meat and then boil the bones to make a stock.

- Get a larger prescription If you take a prescription medication on a regular basis, ask your doctor to write a three-month prescription. Instead of paying three co-pays, you only pay one.

- Use Baking soda for toothpaste It works just the same

- Plan meals that can be repurposed We make a pot roast and make open-faced sandwiches the next day out the leftover meat.

- If you eat out only do so when you have a coupon We decide where to eat based on the coupons we have in our collection.

- Don’t shop for groceries hungry You often end up buying so much more than you really wanted to.

- But generic when possible Store brands foods are much less expensive in most cases and the reduction on quality is not that noticeable except for Ketchup I have never found a generic ketchup that is as good Heinz.

- Watch for thrift store discount days Some stores have a 50% off day and you can get things on the cheap.

- Buy an Entertainment book It will cost you $20-30 but will save you a ton.

- Find out if an item has a price guarantee Some store will pay you back the difference if an item goes on sale shortly after you buy it.

- Always keep your receipts You will need them if you want to get your money back or need a repair

- Remember to send in your rebates Another reason to keep your receipts.

Other

- Adjust your tax allowances There is no reason to give Uncle Sam an interest free loan for the year while you are paying interest on your debt or while you could at least squeak a few dollars out of your savings account.

- Get the most out of your employer Make sure you are aware of all the benefits offered by your employer you can take advantage of. FSA, Tuition reimbursement, 401(K) match, adoptions assistance.

- Go to the second run or Dollar Theater Sure you won’t see it the day it comes out but Hollywood hasn’t been doing much worth the extra expense IMAO.

- Start or join a book club It is cheap and it great entertainment as well as being social with a real live person.

- Quit Smoking it isn’t getting any cheaper and it will save you money in the long run on medical expenses.

- Try grounding yourself for a period to reset your life style “ For a month stop watching TV or playing video games or whatever mindless thing sucks up your time. When the month is over you will find you didn’t need it much after all.

- Offer services instead of gifts A night of babysitting can be more valuable than gold.

What are your best money savers? Tell us below in the comments.

This article contains affiliate links that will pay for this site if you purchase anything through those links.

Is Pursuing Christian Wealth Worth the Spiritual Risk?

I read a lot of personal finance bloggers, many of them Christian. It seems to me that many of them ask “Can we?” in regard to Christian wealth, but rarely ask if we should. Dave Ramsey, for example, talks a lot about handling money God’s way. He says that God’s way will lead to having a lot of money that you can give away later after you are established. Very similar to the prosperity gospel I was a part of; the goal was always to get more money for the sake of God’s kingdom, but it would make us wealthy along the way.

There is no specific text in scripture that says the accumulation of wealth is a sin. However, there are enough warnings given concerning money and the love of it that we should ask if we should be pursuing wealth, at the same rate and with the same intensity as the rest of the world, is really worth it. For example:

Matthew 19 – After telling the rich young ruler to sell all that he has he turns to his disciples and says “Truly, I say to you, only with difficulty will a rich person enter the kingdom of heaven. 24 Again I tell you, it is easier for a camel to go through the eye of a needle than for a rich person to enter the kingdom of God.”

The disciples were astonished because they saw wealth as a direct sign of God’s blessing. If that person couldn’t enter the kingdom then who could? This is because money clouds our vision and prevents us from seeing our need for God’s grace. (And no there is no evidence of a small door called the “eye of the needle” that camels had to crawl through)

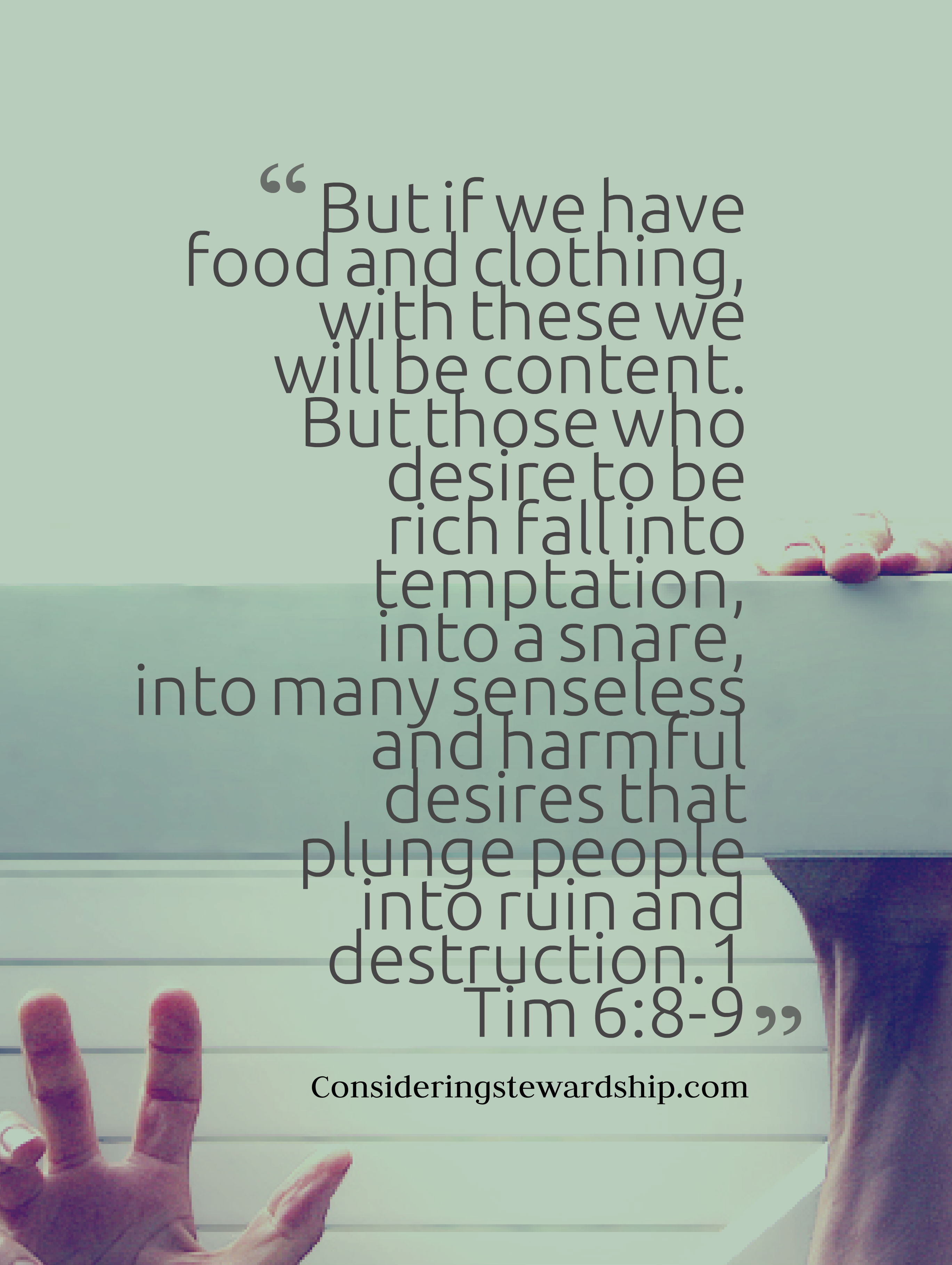

1 Tim –[6] But godliness with contentment is great gain, [7] for we brought nothing into the world, and we cannot take anything out of the world. [8] But if we have food and clothing, with these we will be content. [9] But those who desire to be rich fall into temptation, into a snare, into many senseless and harmful desires that plunge people into ruin and destruction. [10] For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs.

Paul calls to be content with food and clothing because of the inherent dangers in the pursuit of wealth. Of course, we don’t pursue money for it’s own sake. Of all the Christians pursuing wealth, not one of them would say it is for their own sake. Paul seems to be warning a Christian that no longer exists in our day. We only want money for the good it can do, but Paul didn’t seem to be to concerned about our good intentions. He seems to think the risk wasn’t worth the results. The very thing we pursue with such vigor can tempt and draw us to destruction. Is it worth the risk?

I know I am taking a hard stand and I would love to hear your comments below as I process this.

Image by jakerust

Dave Ramsey – My first impression

I have been writing on personal finance and helping people with their money for years, but I have avoided Dave Ramsey like a OSU fan avoids maize and gold. I didn’t want to be overtly influenced by what some people consider the definitive author of personal finance. I realize, of course, that since most of what is taught in the PF world is common sense it all seems derivative, but I still prefer to feel like I am not copying someone else’s work.

been writing on personal finance and helping people with their money for years, but I have avoided Dave Ramsey like a OSU fan avoids maize and gold. I didn’t want to be overtly influenced by what some people consider the definitive author of personal finance. I realize, of course, that since most of what is taught in the PF world is common sense it all seems derivative, but I still prefer to feel like I am not copying someone else’s work.

Dave Ramsey is an Evangelical Christian who makes his name by teaching people “God’s way to handle their money”. I have been asked to assist with facilitating Dave Ramsey’s Financial Peace University, his magnum opus, and so I held my breath and plunged in. It wasn’t as bad as I thought it might be on many levels. Dave is a very polished presenter with a delivery that reminds me of comedian Bill Engvall (they also have the same eyes) his use of humor was engaging and kept me from becoming completely bored, I can’t stand to be on the receiving end of a monologue.

Having said all of that, I am troubled that some of the things he says abuse the bible to prove his way is God’s way. He uses the bible to proof text his points, but has yet to address any passages that would contrast his “God wants you to have the American dream message.” For example, Jesus call in Luke 14:33 “So therefore, any one of you who does not renounce all that he has cannot be my disciple.” Or the fact that the Bible has very little good to say about money unless it is being given away. As a recovering member of the prosperity gospel movement this makes me very nervous.

We are only three weeks into the class so I hope I my mind will be changed as I move forward but I wanted to get my first impression out there before it is too late.

Have you ever taken the course? Tell me if it gets better in the comments below.

Photo courtesy of Jessica Adkins

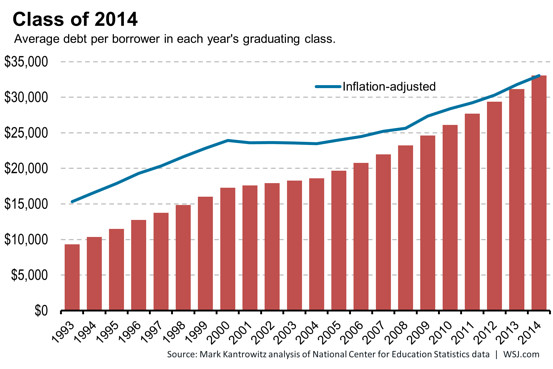

Congratulations to Class of 2014, Most Indebted Ever

The Wall Street Journal says “As college graduates in the Class of 2014 prepare to shift their tassels and accept their diplomas, they leave school with one discouraging distinction: They’re the most indebted class ever.”

I have often wondered if my choice to go back to school was a good one based on my situation. I was 32 and had no degree to speak of, but I was already deep into a career that required a degree. I was very fortunate to get into IT work during the boom when all you needed was a warm body and some aptitude. (which thanks to my parents getting me a C64 when I was 8, I had in spades) Did I really need to go back to school? Probably not, I took on some debt to do it although because of the program I was able to complete my degree in from 0-BA in two years. In working with a lot of college grads who are now turning to a bleak job market I have to wonder how much longer we will swallow the bitter pill of college.

There are some careers are always going to need a degree, but it seems like apprentice programs and boot camps would serve many people better in the log run. If you are going to take out a small mortgage for a career that pays $30,000 a year it isn’t a good investment or good stewardship of your money. I hope things turn around before my girls are old enough to face this ever growing mountain of debt.

HT to: http://ift.tt/UVpGPS

Snagshout review

Snagshout is a social deals website that creates a connection between shoppers and brand owners.

Snagshout is a social deals website that creates a connection between shoppers and brand owners.

Snagshout offers products at discount prices in exchange for reviews of the products. I had never tried to use this type of service before so I naturally wanted to give it a shot. The big bonus was most of the deals you can snag are through amazon so I felt safe in dealing with them. I snagged a pack of 6 micro USB connectors because we lose and break those things all the time. Normally they are 12.99, but with the supplied promo code they were 1.99 and with my Amazon Prime account the shipping was free and two days.

Snagshout made the whole process easy by including buttons directly to he product and the a button to send me to the review page once my purchase was complete. I wrote the review after I had time to test out the cables (which worked fine, it was a simple product) and it was approved by Amazon in moments. For some reason Snagshout had some trouble finding my review and after a three days I simply pasted the URL for my review into their handy field and it was approved by Snagshout a few hours later. The process was clean and easy.

My wife picked up an immersion blender for $10 and had no trouble with her review approval, so perhaps I did something wrong. Let me know if you have issues if you check it out.

The products Snagshout offers seem to rotate in and out, I am seeing items now I didn’t see before and some items I thought to come back and claim are out so it would be good to check regularly and see what they have available.

This post contains affiliate links.

Have Millennials Been Robbed of Their Birthright?

The National Center for Policy Analysis has an interesting article out about the effects of our big government on our newest citizens.

Burdened with an obligation to pay government debt they did not incur, young Americans – those born between the early 1980s and the beginning of the 21st century, or millennials – begin life at least partially robbed of their birthright.

Is this an example of Robin Hood in reverse where the wealthiest generation is taking money from the poorest to support their own lifestyle? Maybe. The bible tell us that a wise man lays up an inheritance for his grandchildren. Not a debt. We are continually forcing our children to pay for things they did not ask for and do not want just to support politically powerful interest groups. That isn’t the biblical model of stewardship.

HT to: http://ift.tt/1IJadZO

When Does Saving Turn into Hoarding?

Over at Christianpf.com they had a good discussion on this topic with some good practical ideas on what to look at. I have a question as a thought experiment. Should Christians have a self imposed (I believe any sort of forced cap would be immoral) income or networth cap? I read about a church that did this for their leadership about 15 years ago. It felt like an over reaction to the prosperity “gospel” of the day and I wasn’t sure how I felt about it. But now I wonder if there is some wisdom in it.

We talk a lot here about how personal finance is personal and much of it deals with a position of the heart, but while we can talk about shades of gray eventually grey becomes black and I have been thinking a lot about where grey becomes black in the case of savings v. hoarding.

The Bible clearly states that saving is a good thing (see Proverbs 21:20) and that hoarding is not (see Luke 12:20-21). But is there a clear distinction between the two? And how can we know if we have crossed the line? There must be a line, but is it completely subjective or not? Should we think nationally where we may be in the bottom 10% or globally where if you are American you are in the top 1% no matter how poor you are?

I would love to have a constructive conversation about this because I process by talking things through. Does the Bible speak to this? I think John did in Luke 3 when he tells the people give one of their coats away if they have 2 and their neighbor has none. My family has more coats than we can fit in our closet! But so do most of our “poorer” neighbors.

So, what would this look like? I have no idea as I said it is a thought experiment and I would love to hear from anyone even if you think I am crazy. Drop a line in the comments below.

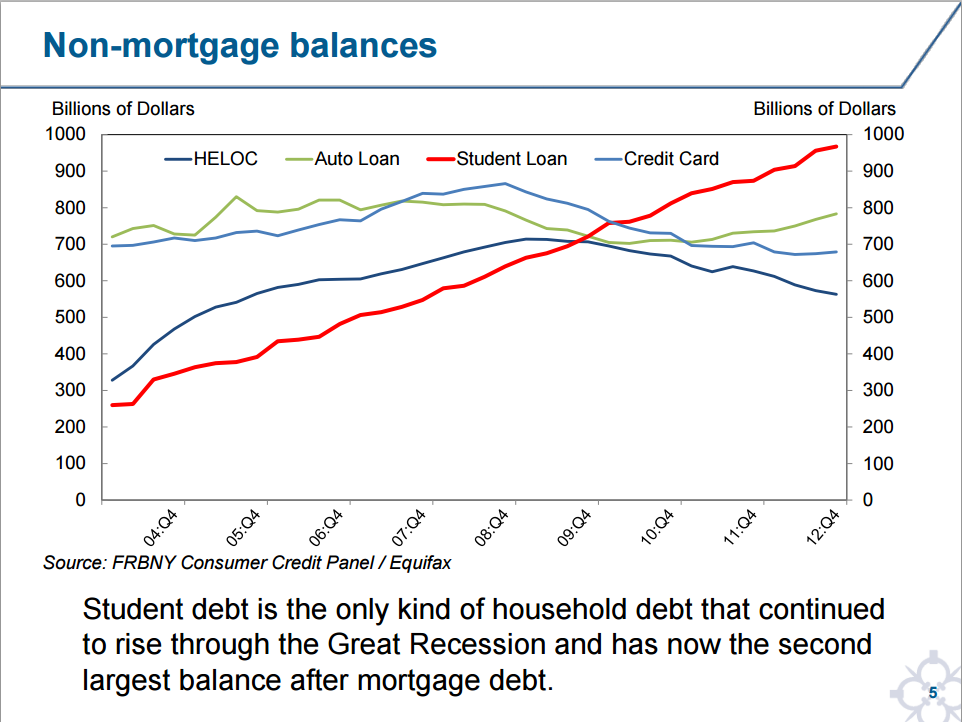

Student Loan Debt Continues to Rise

A new report by the New York Fed shows that while many of us were paying off debt during the great recession. Student loan debt was the only category to continue to rise.

We have a group of young people who are not only going into debt up to their eyeballs and demanding someone else pay for it. They are also being forced to pay money to the richest age group in America through taxation.

Something is going to give here and I am not quite sure what it is, but I don’t think it is going to be pretty.

Source: http://www.newyorkfed.org/newsevents/mediaadvisory/2013/Lee022813.pdf

Fund retirement or pay off mortgage.

I get this question a lot in my classes. It is better to pay off a mortgage or fund retirement? This is one of those decisions that depends on what one means by better, which sounds like a cop out but really it isn’t.

The debate boils down to this…

If your interest mortgage interest rate is 4% and you pay extra on your mortgage you are making 4%. If you can make more than 4% investing you will make more money investing.

But that does over simplify things a bit. And doesn’t answer the question “is it best for you”?”

Mathematically, you can make more money by not paying off a mortgage if your interest rate is low enough and you have a good investment strategy, however that may not be what you mean by this decision. Some people would be served better by the freedom a free and clear house can bring. Maybe you want to start a business or change careers or go into the mission field. Having a free and clear house could make that much easier.

Folks like Dave Ramsey are big proponents of paying off your mortgage, it is one if his big steps in accomplishing financial peace. And I think I would argue that it is probably best for most people, simply because most people aren’t good at managing their money.

Thoughts from around the web…

http://twocents.lifehacker.com/money-advice-the-experts-don-t-agree-on-paying-off-you-1607494999

Pay Off Mortgage Early vs. Save More For Retirement? Digging Deep Into The Details

Image by stevensnodgrass

Money dangers in your 30s

I have posted previously about how to screw up your finances in your 20s. And now that I am half way through my 30’s I can see a few money dangers that I would like to warn you about. My wife and I started to notice some things in how we looked at money and maybe this isn’t about how old you are, but how long you have been taken personal finance seriously. I feel like we are hitting a point of frugal fatigue. I have been frugal for a long time now, most of my adult life actually. And there are days I am getting quite tired of it.

Here are some dangers to look out for…

- Spoiling your child – We were determined not to do this, in fact for the first 6-8 years we really didn’t buy much for our girls. We were very blessed by friends who gave us a lot of toys and grand parents that did most of the new buying. Recently, however we are finding that our girls have A LOT of stuff. We even started storing bins of different types of toys in the garage and rotating them out so they would play with different things. Kids don’t need as much as they want. It is easy to try to give them more and more stuff, but they want your time and attention more.

- Spoiling yourself – This one is actually harder money dangers for me than spoiling the kids, at least right now. We are still struggling with the right decision for our house. It is nice to look at all the big new homes that we could “afford”, but are obviously able to live in something smaller. Our (my) pride is pushing me to buy a bigger house than we need. It is easy as you are coming into the prime of your career to want to buy more and more but this is the time to stay the course and live simply to help those in a world of need.

- Ignoring Insurance needs – Look, no one likes to talk about this, but if you have a growing family you need to look at insurance. Life insurance is meant to take care of your family if something happens to you. Do you really want your spouse struggling to keep your home and your family together? You should really chat with an insurance professional and decide what is best for your family.

- Ignoring a will, POA and survivor checklist – along those same lines, if you have a family and don’t have a will, “shame on you”. You don’t want your spouse struggling over decisions surrounding your death, or arguing with your family over who gets what or who has power of attorney. Anyone can make a will and power of attorney through Legalzoom or prepaid legal. Also if one of you takes care of most of the money matters, you need to let your spouse know who to contact and where the money is located along with passwords for those accounts, and all the other information they may need. Check out how you can use lastpass to make that easier..

- Still having consumer debt – Come on now, it is high time you paid off those mistakes from your 20s. Debt can keep you from pursuing your long term goals, and can cause rifts in your marriage that you don’t want to have to deal with.

- Not funding retirement – It is closer than you think. Retirement needs to be planned for, some would say it is even more important than a childs education planning because there are scholarships for school, but not for retirement. Time and compound interest is still on your side but you need to start sooner rather than later.

What are some mistakes you think make your 30’s harder? Let us know below.

Other articles around this same topic…

image by flickrohit