Christmas Spending Is a Test of Your Treasure

David Mathis over at Desiring God wrote a great article about how we regard money this time of year. It is worth the read just to challenge yourself on the idolatry of money. It is really hard to not spend money on things this time of year. But we are not called to spoil ourselves or our children. We are called to honor Christ. I do believe you can do that by giving gifts because that reflects the time when God gave the gift of himself but it is a fine line to not go overboard.

Not only are we on gift-expectation overload with Christmas, but then comes the year’s end and that one last chance for tax-deductible charitable giving. December bids us dig deeper in our wallets than any other season.

HT to: http://ift.tt/12OET8W

Looking for a new house

So, my wife and I have been looking into buying a new house. We have been living in our “starter home” for over 10 years now. We didn’t intend to be in it this long and with two growing girls we feel like we need to move on and get something a little larger. What are our considerations?

Are you creating an idol in our new house?

We think there is a distinct possibility that we may be looking for a house to provide peace that only God can provide. Although we do want to show more hospitality it is very easy for a new home to consume more of your life than it frees up. I have recently had a conversation with a friend who asked me if it was possible his house had become an idol of sorts. The question is why do we want a new home. We need some more space for our family including more in the ways of storage. We would like some more land in a more rural area partly so we can enjoy some peace and partly to enjoy activities that require more space, like archery and four-wheelers.

How much can we afford?

This is another big question. According to several calculators on the subject we can afford anywhere between 180 and 350k. Which is crazy! I couldn’t imagine making that kind of mortgage payment. We have a budget in place now that allows us to be fairly generous with out money while putting some away. Moving will mean we need to adjust out budget accordingly and we need to understand those changes. So the question is not “What can we afford?” but “How do we want to spend God’s money?”

Should we even move?

This is the question I really don’t want to ask myself. We have some great neighbors and our church has just planted a new congregation in our neighborhood. (after 5 years of driving 25 minutes to church). We could stay in our home and pay it off faster while keeping a lower mortgage payment and keeping more freedom in our budget.

Space is subjective I suppose, we feel cramped, but according to this article living space per person has doubled since 1973. Maybe our culture is just telling us that we need more space.

These are some of the questions that I will be reviewing over the next few months or until we make a decision…

Image by Jan Tik

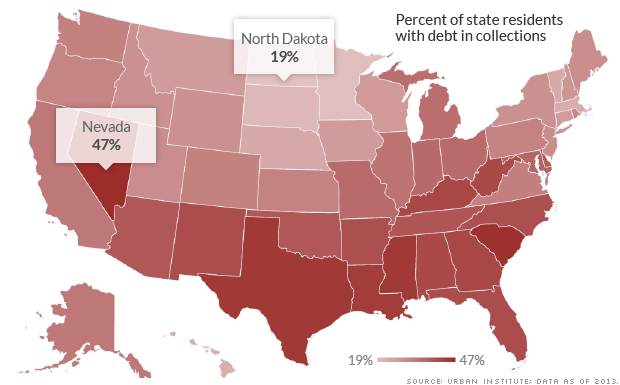

1 in 3 American adults have ‘debt in collections’

This is a pretty scary number. This is why being a good steward of your finances is so important.

Debt in collections by state

Americans have a debt problem. An estimated 1 in 3 adults with a credit history — or 77 million people — are so far behind on some of their debt payments that their account has been put “in collections.” That’s a key finding from a new Urban Institute study.

HT to: http://ift.tt/1nC2iSX

Balance Giving vs Investing

When I get to the Q&A portion of my classes there is a question I always get. “How do you balance giving and saving/investing?”

I wish I had a straight answer for the question of giving vs investing, but any short answer does a disservice to the question itself. As believers we are called to give sacrificially and generously to those in need. And it is a part of our culture and even sensible to save money for things like retirement. If you are looking to build a retirement nest egg and give sacrificially it can be a struggle to find any balance between them.

Obviously this isn’t an easy question to answer but here are a few things to consider.

-

Are you living sacrificially?

Take a look at your budget and your spending and ask “Is my giving impacting my lifestyle?”

CS Lewis put it this way:

I am afraid the only safe rule is to give more than we can spare. In other words, if our expenditure on comforts luxuries, amusments etc is up to the standard common among those with the same income as our own we are probably giving away too little. If our chartities do not at all pinch or hamper us, I should say they are too small. There ought to be things we would like to do but can not because our charities exclude them (Mere Christianity)

-

Retirement isn’t biblical

This is a concept most people don’t realize. Retirement isn’t something the bible even addresses. Retirement is a twentieth century invention and it was created to force older workers out of the system so they would stop slowing down production. The only way to do it was to pay them not to work. Now it is just assumed that we will get to stop working one day even if we can’t afford it.

We may need to save for the loss of income as we reach retirement age, but shouldn’t assume that there will come a time where we are not working.

-

Giving in light of God

As Christians we should think about our giving in light of God as the great giver. God planned to show his goodness to us before the foundation of the world in giving his son to save us. Jesus models for us what type of sacrifice we are supposed to display.

Philippians says “Have this mind among yourselves, which is yours in Christ Jesus, who, though he was in the form of God, did not count equality with God a thing to be grasped, but emptied himself, by taking the form of a servant, being born in the likeness of men. And being found in human form, he humbled himself by becoming obedient to the point of death, even death on a cross.” Phil 2:5-8

If Jesus was willing to set aside equality with God we can be willing to set aside equality with our neighbors’ standard of living.

Good Guy Discount

This goes along with other articles I have written about negotiation. This American Life had a act in one of their shows where a man discussed is “Good guy discount.” I have always loved the concept he discussed, but this gave me a great method to ask for a discount without coming off like a jerk.

I ask for the “Good guy” discount. It has worked 100% of the time so far. Granted I have only tried it twice, but that doesn’t change the success rate.

At the Cincinnati aquarium I learned that our local Zoo was no longer part of their reciprocal discount program. They used to be but had neglected to sign up this year. So, I said “OK, just give me the good guy discount then.” The girl behind the glass laughed and asked if I was an alum from any of the local universities. Which I wasn’t. Then she moved onto other organizations; she must have gone though 10 or 15 until she finally found a way to give us a 20% discount on our 4 tickets.

Asking for the “Good guy” discount disarms the person you are talking to with humor. Obviously, they won’t have a “Good guy” discount but I find they will do what they can because you ask. A lot of places have a plethora of discounts available and even if you don’t qualify for one you may get it just for asking.

Plus as an added bonus you don’t have to feel embarrassed if you are asking for the “Good guy” discount because you can always laugh it off if it gets awkward, but it never hurts to ask.

Image courtesy of Cubmundo

My kids come first?

This stems from a discussion I recently had on Facebook. It isn’t in my traditional category of personal finance, but it is about stewardship of a different kind. Something very important that we steward is our children. Our kids are in our complete care for temporarily before they come into adult hood. For some time and in some ways their relationship with the Lord is mediated through their parents until they are old enough to build one on their own. However before the throne of God we will all be equals, there will not be the hierarchy of family like we have here on earth.

Therefore, we are stewards of our children in as much as they are a gift from God given to us to raise for a short period of time. This is something very important to remember when considering how we raise our children.

I pointed out on Facebook that there is something more important than our relationship with our children, and that is the relationship we have with our spouses. Someone posted the picture above and I pointed out that my wife comes before my kids. A lot of people think that kids come first and should but I have to disagree. I have caught a little flack for this stance but based on my biblical understanding I can’t see it any other way.

Genesis 2:24 says “That is why a man leaves his father and mother and is united to his wife, and they become one flesh.” Children will leave their family and join in a special union with their spouses. They become one in a way that I am not one with my children. Many marriages start to focus so hard on their children when they come along that they allow their marriages to fall apart. It is why you see many divorces after the kids leave the house, the marriage has taken a back seat to the children and is an anemic version of itself.

Your relationship with your children is immensely important, but understand your marriage is more important, it is the foundation of the family to which your children belong. It is structure where they will learn about the Lord, and about love and covenant, before they ever read scripture for themselves.

9 ways to save money with kids.

Here are 9 great ways to save money with kids.

- Create a Babysitting Co-Op No not like those books from such a long time ago but if you and another couple can exchange babysitting services it will give both of you a free night out. You watch their kids this week they watch yours next week. Now you can have date night without paying cash for a sitter. This is great for your marriage as well as your wallet.

- Hand me arounds There is no reason to buy all new clothes for your child, especially when they can only where the same thing for a few months before they grow out of it. When you are done pass them along and find someone else to do the same with. My wife has a Mothers group at church that constantly passes clothes around and saves everyone a ton.

- Play at the Public Park Why not just go to the park and play with other kids, you already paid for it.

- Watch the local parks for educational programs Take your kids to these and they may have so much fun they won’t even realize they are learning.

- Public Libraries There is so much that can be had at public libraries from internet access to the books and learning programs.

- Use city services There are plenty of free (already paid for through taxes) activities for children around our city, between Metro parks and libraries there is plenty to keep them entertained.

- Watch local churches Especially in the summer there are tons of Vacations Bible Schools for kids’ activities.

- Stop spending so much on your kids Really they want your time and love more than anything. Make up games you can play at home all the time or just play tag.

- Buy in bulk and pack your own snacks. Our kids know if we are gong to the museum or the Zoo they are carrying their own food and we don’t buy it there. We taught them how much things cost and now our kids see prices and ask “Who would pay for that?”

What are other great ways you save money with your kids?

You should always have a car payment.

You should always have a car payment. Unless you live somewhere like NYC where you don’t need a car, then you can move on to another one of our great articles. You should always have a car payment, not so you can drive the newest model every year, that would be crazy. However, most of us are in a place where we will be needing a new car sooner or later. How are you going to pay for that car without going into debt and taking on a few hundred dollars a month?

Always have a car payment and make it to yourself.

If your car is paid off, find some money in your budget and dedicate it to your car fund. Even if it is just $50 or $100 dollars a month it will help a lot in the long run.

Think about it. If you take out a loan for a $10,000 car and you just pay the minimum you are paying around $2000 in interest over the course of the 5 year loan. That is 20% increase in the cost of the car. Would you have paid 20% more for your car up front?

Every thousand dollars you put down saves you close to $200 in extra interest. And perhaps you can even save enough to not need a loan in the first place. If you take good care of your car there is no reason why you can’t pay cash for your next one.

This habit also prevents lifestyle creep. If you always have a car payment you never get used to living without one. Then if you really did need to take out a loan you don’t won’t feel the squeeze in your budget, because the payment is already there.

I am a fan of driving a car as long as you can, but I will admit I don’t feel like taking that route with my wife and kids so perhaps she can get a newer car before I do.

Financial Samurai has a great article on how to determine how much you can spend on a car. It is an interesting idea but I am not sure how practical it is if you try to live it out. It would definitely help to prevent getting in over your head.

How to help kids manage money

How do you help your kids manage money? This is an article where I don’t think I have the one right answer. My girls are still young and have trouble understanding the value of money. We have tried a few things to help them get the concept, but I think these ideas are all part of the whole and not magic cures in and of themselves.

We are open about money with our kids.

My wife and I have been fairly open about how money works and the value of it. (Although because kids talk I still haven’t told them how much I make.) We explain that everything costs money and how much. I explain that God has blessed me with a job to be able to pay for our home and our food. We tell them how we give to the church regularly and the other ministries we sponsor. My wife takes them shopping and they understand the cost of items. When they ask why things cost money I explain how capitalism should work and how it should be a win-win for everyone. They have a few business ideas I need to encourage because of these conversations and a few episodes of Shark Tank.

We give them their own money

Well they work for it. They earn tickets for doing their chores which can be traded in for money or screen time. Their money is divided into a three part bank for giving, spending and saving. Any money is spending is theirs to do with that they please. (Although it is really hard when they want to buy crap.) Saving money must be targeted to a larger purchase they are working towards. Their giving must be directed outside of our home to church or to something else like the girls we sponsor through compassion international.

This is hopefully setting a pattern in their life. They are able to save money and delay gratification. They love to give money to good causes and have even thought of a few creative causes on their own. This is great because it gets them thinking about someone besides themselves.

We show them the water

You remember the saying, you can lead a horse to water? We show our kids the wise choices and explain them to them as best we can but we still let them make bad choices. “You can buy ice cream from the truck or you can buy a whole box from the store at the same price.” It seems to be working more and more as our older daughter is talking to us about her thought process and the smarter choices. I am sure they won’t always make the right choices but who does? We have let them suffer the consequences of their bad habits so they will hopefully learn a lesson down the road.

Did you parents do anything to help you understand money? What worked what didn’t work? What will you do with your kids? I really want to know because I don’t have the answers on this one.

Image by goodncrazy

Cash as a commitment device

What is a Commitment Device?

What is a Commitment Device?

Never heard of a commitment device?

A commitment device is a choice that an individual makes in the present which restricts his own set of choices in the future, often as a means of controlling future impulsive behavior and limiting choices to those that reflect long-term goals.

The most interesting example I heard was of a man who wanted to lose weight and so we took embarrassing pictures of himself and gave them to a friend who promised to publish them if he did not meet his weight loss goal. Just having a budget it a way to control the actions of your future self. It allows your logic to take control before you emotions get out control.

Cash as a Commitment Device

Cash can be a more serious method of keeping spending under control. Unlike a credit card or even a debit card, cash holds a hard line on your spending. Once the cash is gone you can’t spend any more of it.

We use an envelope system for certain parts of our budget that we don’t use automatic bill pay for.

- Groceries

- Household

- Personal Care

- Dining Out

- Kid’s Allowances

We use cash for each of these categories for some different reasons. Groceries/Household/Dining out – to help to control spending. Personal care/Allowances – Because money comes out of those at irregular intervals, but I don’t want to spend the money in other places by accident.

There are people who use cash for all of their budget, but for us that seems like a bit of overkill. We have found that for these categories it works perfectly for us

Image by 401(K) 2012