1 easy way to save a grand in a year; reduce your property tax

Almost a year ago I stumbled onto a little company called ValueAppeal. They offer to help you file to have your property tax reduced based on an overvaluation of your property. I have finally gotten through the process and am ready to do my Valueappeal review only to find out that they dropped that part of their business. But the good news is, anyone can still fill out the paper work and challenge the valuation of their property.

The time when the usefulness is getting shorter as property values are beginning to rebound from the recession, however it may still be worth your while if you want to pay less in property tax to look at properties around you and see if they are worth more or less than yours

Property Tax basics

Property taxes are taxes on real property (usually homes) which fund schools, and other services for a county or region. They are based on the real or perceived value of the property.

If you decide to go through this process it is not a time to be emotional, you don’t really want to admit that your home is not worth as much as your neighbor but the reality is there are more factors than you can control that contribute to the value of your home. Most taxing districts allow for some sort of process to object to the value of your property, you may need to fill out some paperwork and perhaps attend a hearing. But it is possible to save thousands of dollars a year. I was able to save over $1500 dollars. Which will be helpful if we need to rent out our current property.

Image by danmoyle

Everything can be a pre-tax deduction

A Pre-tax deduction refers to things done the governments preferred way that reduce the amount of income you pay taxes on. For example if you make $50,000 a year and you put $10,000 into a 401(k) (one of the governments preferred savings methods) then you will only pay taxes on $40,000 a year. This is a nice way to reduce the amount of taxes you pay at the end of the year and with things like a 401(k) the money is taken out of your paycheck before you see it, so you never even have the contributed money. Not only does this prevent you from missing a deposit to your retirement it makes your taxes simpler because you employer tells the IRS that you only earned 40,000.

Post tax deductions are things like mortgage interest, IRA deductions etc that are tax deductible, which means (Normally) when you pay $5,000 of mortgage interest you will get the tax you paid on that $5000 back at the end of the year. This is what we call a tax refund, it is money you over paid to the government throughout the year. It is like getting change at the grocery store, only you have to wait months and fill out a lot of paperwork to get it.

Both post-tax and pre-tax deductions are tax deductible, which means you do not have to pay taxes on them. The difference is that you don’t get all of your money from post-tax deductions up front. The government still taxes the money and then gives it back to you when you file your taxes. Maybe you don’t mind giving Uncle Sam an interest free loan or think he can spend your money better than you can but I don’t think so.

When I moved to my new job recently I was disappointed to learn that they did not do a matching 401(k) contribution. In order to make up for my disappointment they offered me a signing bonus (read onetime bonus) I asked for that money as part of my salary(so I could have it every year), which they were happy to do. (Always negotiate your salary and benefits) I had intended to roll over my old 401(k) to the new one for my company, but instead decided to roll it into a traditional IRA with my old friends over at Fisherwealth. (To the best of my knowledge no relation, but we have done business together for years). I can now take the money I negotiated and deposit it to my new IRA. But, what am I to do about the money being a post-tax deduction? I am being taxed on that money even though it is tax deductible.

This is when I realized that if you know how things work you can make almost anything a pre-tax deduction. When I started my new job they asked me to fill out a form to determine how much money the federal and state governments should take out of my income every paycheck. To pay my taxes. Now this isn’t a nice simple form like take out $100 per check, no it is a complicated formula so you most people don’t realize what is going on. But, as I have written about here, you can get your tax refund all year long by filling out this form properly.

This way all your tax deductible expenses including your child credits etc, can be pre-tax. The IRS has a handy little calculator to determine how to eliminate your federal refund and get the most out of your paycheck. It is here if you want to check it out.

Do you prefer to get a big refund or a bigger paycheck?

Image by irsein

Ways you are wasting money

There are tons of places we all waste money every day. Here are some big ones I have learned about the hard way. Check the list below and see if you are wasting money with any of these.

- Giving Uncle Sa

m an interest free loan – Why should you let the government hold onto your money all year only to give it back to you interest free? Check out our article on “Giving Yourself a Raise” for more details.

m an interest free loan – Why should you let the government hold onto your money all year only to give it back to you interest free? Check out our article on “Giving Yourself a Raise” for more details. - Carrying a balance – If you are have $1000 on a credit card at 19% you are paying $190 a year in interest. That same money in a savings account would earn you about $19, if you are lucky.

- Ignoring little things around the house – Small issues around the house may lead to larger issues if not resolved. Fixing things earlier will save you money.

- Not giving to to your 401(k) – Make sure you understand how your companies 401(k) works so you can get the most out of it possible. If your employer will match any part of your contributions you are leaving money on the table by not contributing. There may be other employer benefits you are not taking advantage of.

- Paying bank fees – It happens to the best of us, we forget to pay a bill, (Which is why you should automate your finances) or you overdraft.

- Leaving money on the table – Ever gotten a rebate you didn’t follow up on? Ever added money to an online service you stopped using and left the money there? I have I still have $25 in a Pokerstars account and a few dollars of credit in some other places.

- Policies that don’t fit your needs – You may be paying more than you need to for an old policy that doesn’t fit your needs. Are you paying extra for a low deductible? Or are you missing discounts you didn’t qualify for before?

- Driving stupid – I always laugh at the people who speed around me just to sit at the same light I was already slowing down for. So much gas (and therefore money) is wasted by stupid driving and poorly inflated tires.

What other ways do you see money being wasted? Tell me in the comments, I would love to hear from you.

How to compare job offers

Weighing Tough Decisions

When you are faced with a new job offer (other than being extremely blessed) you may be in for a rough ride. How do you make such an important decision? How are you to compare job offers? If you are like me you may try to analyze and quantify every detail of each position in order to make a decision. It can be difficult and there are a lot of things to think about. This article will hopefully assist you with such a decision.

I have just gone through this process myself so it is clear in my mind.

The Intangibles.

Obviously there will be things you can’t quantify. If you have a really great relationship with your coworkers. (or a really bad one) If you are working for a non-profit that is really important to you. These are things that you can’t convert into a formula to make a decision so for the sake of this article I am going to ignore them. You will have to determine how important these things are for yourself.

Base Pay

This is the easiest to compare and the largest portion of your compensation. This is easily examined simply by looking at what they are going to pay you if you are salary or by doing some simple math if you are hourly. Hourly rate multiplied by 2080 gives you a yearly rate assuming no overtime.

Insurance costs

Having just lived through this I learned that my old employer had really great insurance rates and where ever I went I was looking at doubling my insurance costs. Always ask for this information before accepting a new job you may learn that you have actually taken a pay cut because an increased cost of insurance has eaten up your raise.

Vacation

Starting over in a new job often means that you are losing paid time off or vacation. I compared this by multiplying it by my daily salary rate to determine how much the vacation was worth in dollars.

Commute

The book “Your Money or Your Life” is great for helping you see all the costs associated with your job, including commute and clothes. The IRS millage rate for 2014 is $.56 so take your commute and multiply by this number to make sure you won’t be losing money in the cost of driving.

Additionally, I tried to quantify the hours I was going to spend in my commute. One of the offers I was looking at put me far away from home and into heavy traffic so my actual commute would have been longer than the millage lead me to believe.

401(k)

The match, if any for your 401(k) can be a large difference between two jobs. If your current jobs matches 50% of the first 4% of your salary and your new job doesn’t offer a match then you are giving up all that tax free money.

Other Extras

There may be other offerings from your employers, some of them get very creative to attract top talent. What else do you think you should examine?

Image by winnifredxoxo

Satisfied In The Lord, Not A Paycheck

It was a while ago that I wrote “Please Give me my Idol“, an article where I talked about my personal idolatry in seeking a new job. Well, I had been seeking a new position for almost a year when God dropped two offers in my lap almost at the same time. It made me stress more than I have in my life, as I tried to use my own wisdom to make the decision instead of trusting in the Lord, because that is how I roll.

I essentially got the raise and promotion I had wanted, which is a blessing, but I have been wrestling with my own sinfulness in the process. How much do I rely on myself and my abilities instead of relying on God. How much of my career ambitions are sinful in nature as opposed to simply wanting to work hard and represent the Lord well. I understand that well paid or not I should be satisfied in the Lord; it is just really hard to do.

When I first started to talk about my job search, almost a year or more ago, I was discussing it at community group. Talking through why I wanted a new job and more money. I said when it comes to my career I really only wanted to go one more step. I feel that if I pursue my career further it will be too difficult to maintain a work/life balance that is important to my families well being. An uncomfortable conversation followed that statement. I am not positive who it was with, but I remember the conversation well:

Me: I really only want one more promotion, then I will be in good shape.

Someone: Until you get that promotion.

Me: No, I think I will be good

Someone: Until you get that job.

I got what they were saying, but thought they were wrong. Until I just found myself planning my next career move after just receiving that promotion that I was so sure would be good enough. It is possible that my heart may be pure in this matter and I am in a different place in my career now. That being said, it is best to examine my heart and pray asking God to reveal any sinfulness in this area. I know that I am not satisfied in the Lord nearly as much as I should be. I know I rely on my self far to much.

That being said, sitting down with some friends of our who are missionaries really opened my eyes to the reality that my money is to be used to further spread the gospel. The reason God would bless me is not simply to hoard the money, but to use it for his glory.

Being satisfied in the Lord is something we give lip service to but it is difficult in a culture where you are constantly being told what you need in the form of commercials. If we could only have the life they promise us. The fact is all those trinket will pass away and be trash at some point. Only the things that are eternal should be pursued to the degree we chase a better lifestyle. I want to be satisfied in the Lord but I don’t want to have to go through losing everything in order to learn that lesson.

Image by famzoo

No Article This Week

I have been going t hrough some crazy personal things, this week. I know this is how blogfade starts, but that is not the case here. I actually have 4 articles I want to write based on things that are happening to me and my career, I just haven’t made/had time. I would rather not put up something just because I should. I want to put up something of quality instead.

hrough some crazy personal things, this week. I know this is how blogfade starts, but that is not the case here. I actually have 4 articles I want to write based on things that are happening to me and my career, I just haven’t made/had time. I would rather not put up something just because I should. I want to put up something of quality instead.

So, if you would like something to read may I suggest some of our specials of the day:

Give me my idol – This is be relevant for the new articles I will be writing shortly…

Questions about money before marriage – Marriage season is upon us, even if you are already married check out these conversation starters for you and your spouse.

100 money saving tips – Always helpful…

Image by adventur

My extra income adventure: A New Series

I am going to be kicking off a new series on this blog. I have been interested in producing some extra income in my life in order to help to pay for the down payment for my house. I have often looked into passive income ideas and it seems like most of them are anything but passive. Passive income is income that you don’t directly trade time and labor for money. Examples would be royalties, or licensing etc. Although my book would fall under this category I don’t have any delusions about making millions of dollars from it. (although it would be nice)

I am going to be kicking off a new series on this blog. I have been interested in producing some extra income in my life in order to help to pay for the down payment for my house. I have often looked into passive income ideas and it seems like most of them are anything but passive. Passive income is income that you don’t directly trade time and labor for money. Examples would be royalties, or licensing etc. Although my book would fall under this category I don’t have any delusions about making millions of dollars from it. (although it would be nice)

I had considered getting a second job, but didn’t want to give up time with my children who I only see 3 hours a night as it is. So, one of my qualifications for these ideas is that I am not simply trading my time for money directly. (I will do this job for x dollars) I hope to find other ways to work once and make money over and over with that work. I plan on doing some of this by outsourcing some of the work that I can’t do, or don’t have time to do. If I do my calculations correctly the Virtual Assistant (VA) should pay for themselves.

I have some money that I am able to invest in business ideas to capitalize a few of them, which makes me fortunate. If you want to see this done with almost no money check out UpwardsofTwenty. He is starting with $20 dollars and investing in interesting ways to grow from that $20 to where ever he ends up.

My plan is to start with some small ideas that I can put into place once and make more than an hourly wage in the process. I am not going to throw my money at any get rich quick schemes, that would be bad steward ship although even those crack pot ideas have real extra income ideas as their kernel of truth.

After I have completed my first venture I will update you with the plan I followed and the money I made. I plan to be as open and honest as I can with this part in the interest of transparency.

In order to keep myself sane I am going to look at any money invested that loses money as the cost of education. I find that I am very hesitant to take risks but hopefully I can break myself of that mindset with some small victories.

There is no right way to do personal finance

People have to find what is for them and what works as far as personal finance goes.

There is no one way to do personal finance.

Tax Code War on Women

The real “w

ar on women” is in the U.S. tax code, says Diana Furchtgott-Roth, director of Economics21 at the Manhattan Institute. Single working women face higher tax rates when they marry, a reality that discourages marriage or encourages women who do marry to quit the workforce. When married women decide whether to enter the labor force, “their tax rate begins at the rate on the last dollar of income earned by their spouse,” Congressional Research Service specialist Jane Gravelle explained in a Senate Budget Committee hearing.

This article by Diana Furchtgott-Roth is an interesting read and is something young couples should consider when determining things like if and who will stay home with children. This appears to assume that Women are the secondary income earners in their family which may be mostly true but not always.

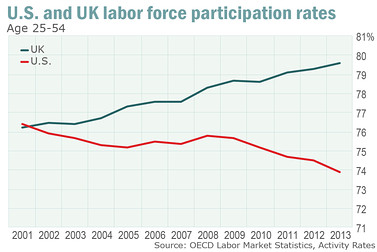

Currently, the U.S. tax code discourages work, discourages marriage and encourages women not to advance. This is the real problem for women that politicians should focus on.

Of course the tax code also discourages men from working in some cases, but the penalties of marriage do seem to practically hinder women more. The chart above compares US and UK women’s participation rates. The UK does not have the marriage penalties that the US does because couples still file separately and have their own deductions. All in all it was an interesting read for someone who is not a big “Women’s Studies” kind of guy.

HT to: http://ift.tt/1hoH2wI