Preparing for Christmas early.

Now that the Christmas season is over you may be asking yourself “How am I going to do this better next year?” Preparing for Christmas can be easy if you know what you want to do.

Many of us get carried away with the “Christmas spirit” and spend more than we intended to. Maybe this is even done with the best intentions, we love the people we are buying for and we want to bless them but there are smart ways to do it and not so smart ways.

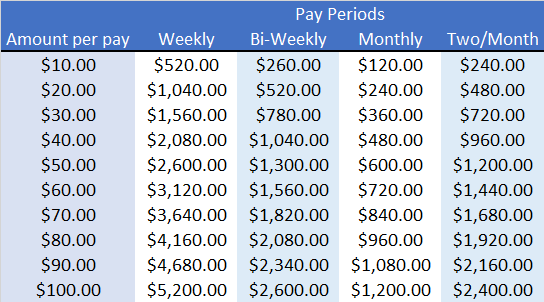

- Start a Christmas account – Many banks still offer these accounts you setup your direct deposit to do a small amount every

paycheck and then they mail you a check in October. We don’t use a traditional “Christmas” account but a simple savings account from Capital one 360. We just pull out the money we will need come shopping time. The table to the left can show you how much you can save based on your pay period.

paycheck and then they mail you a check in October. We don’t use a traditional “Christmas” account but a simple savings account from Capital one 360. We just pull out the money we will need come shopping time. The table to the left can show you how much you can save based on your pay period. - Plan ahead and buy at the right time – Prices fluctuate throughout the year depending on the product. Air conditioners are less expensive in the winter than they are in the spring. If there is a larger ticket item that you know you are going to buy for the holidays plan ahead and buy it when it is cheapest. How do you know when things are cheapest? Lifehacker had you covered.

- Determine your plan – Do you need to buy for everyone you know? Or even everyone in your family? No you don’t. You can trade names and do a secret Santa, so you can buy one gift that matters instead of a couple of dozen gift cards. We have decided to do a “Want, Need, Wear, Read” approach within our family so we are limiting the items we are exchanging. Hopefully this will prevent crap from building up in our kids’ play room.

- Work the system – This takes a little bit of work but you can buy gift cards to buy your gifts and get rewards for doing so. Our local Kroger offers discounts on gas when you spend money at groceries, including gift cards. We do most of our shopping on Amazon so we first go to the store and buy gift cards. Then we get discounts on the gas we will use to go over the river and through the woods to Grandmothers house. If you are disciplined enough you can even use a rewards credit card to get some rewards that way.

Christmas doesn’t have to be stressful if we plan ahead what steps have you taken or do you want to take in order to be prepared for Christmas next year.

Image by decar66

This post includes affiliate links to companies that may reward me if you click them.

Why you and your spouse should have the money talk.

Recently, my wife and I have been slacking off on our money talk. I am the money nerd in our family so I track most of the data and I wanted to get back on track with keeping her in the loop.

1. The money talk keeps you accountable

It is easy to get sloppy with money. I am guilty of using more money than I should to by special treats for my family. Having a consistent money talk with my wife keeps me accountable. I know I will have to talk to her about those little treats. It makes me think twice and helps to keep us directed toward our goals. It isn’t that I am hiding bad things but those little treats are working against our goals.

2. The money talk keeps you on the same page.

It is easy to put the budget on cruise control. But, things can get out of line easily. Having the money talk will make sure you and your spouse are on the same page. It makes sure that the goals you set at one time are still the goals want to be pursuing. It gives you the opportunity to review and change those goals should the need arise.

3. The money talk brings you together.

This one was a big one for us most recently. I felt like I had let my family down by making some minor mistakes with the budget. We have a pretty complicated system and it is hard to manage sometime. Having the money talk was hard for me because it required me to admit I had made the mistakes and seek my wife’s forgiveness. It was tough on my pride, but it brought us together as a couple

Bottom line the more you talk about money the smoother it will go if you both are walking in grace.

Do you have any tips on how to have this conversation?

Image by kabaldesch0

100 Money Saving Tips

Here are 100 money saving tips you can use to pay off your debt, give or save to invest. If you like it please share on your favorite social network.

- Adjust the Thermostat In the summer turn it up and in the winter turn it down. You will use less energy. Get a programmable thermostat if your house is empty during the day; you can save a lot of money and still have the temperature you want in your house before you get home.

By Jess from Canada (HPIM4771) [CC-BY-SA-2.0], via Wikimedia Commons

- Cut the cable Cable TV is becoming increasingly expensive as well as increasingly redundant since most networks are putting their content online, either on their own websites or on sites like HULU.

- Combine it if you can’t cut the cord then at least find out if you can bundle the services and save money in the process.

- Threaten to cancel and see what kind of deal you can get; Cable companies are striving for subscriber numbers right now and just want to hold onto their current clients. You can get a greatly reduced rate if you just tell them you want to cancel.

- Entertain at home A game night or a nice dinner is much cheaper and nicer in many cases, when done at home. Find other like-minded people and find creative activities.

- Learn how to sew a button Don’t throw away clothes because of minor issues. Sew the button back on if you stain your jeans or rip them make them your yard work jeans.

- Make gifts don’t buy them Making quality gifts takes time, but the person getting the gift may appreciate it much more.

- Convert to a gas or an instant water heater They are more efficient and can save a lot of money over time.

- Replace incandescent bulbs with CFL although there is some debate on this you can test and see if it helps you save money.

- Get rid of your home phone With cell phones being what they are now there is very little reason to have a land line. If you don’t get the best service at your home many cell phone providers will give you a device that will boost the signal in your home. It is like having a tower in your house.

- Shut vents in unused rooms This may not be a good idea if you have forced air heating, but shutting vents in unused rooms can save on your heating and cooling bill.

- Change the filters in your home every 6 months This makes your HVAC work more efficiently

- Use a power strip to turn off your entertainment system There is a term being used call vampire power where a lot of new electronics draw small amounts of power even when they are turned off. Using a power strip can eliminate that power draw and save you money.

- Buy used when possible Pay extra for a used quality product instead of a disposable quality product. Especially when it comes to kids items that they will outgrow in 6 months.

- Get live in help If you have a spare room you can rent it out to someone you trust.

- Pay your mortgage on a bi-weekly schedule Doing this can shave years and thousands of dollars from your mortgage.

- Clean your own carpets You can rent the machine or borrow it from someone.

- Attend College online It is much cheaper to get your education online just do your research and find a good school. I just finished my degree in 2.5 years.

- Delay purchases When you have a desire to purchase something wait a few days maybe even 30 to make sure you still want to spend the money on it.

- Buy a Clothes line Running a dryer costs a lot of money. This can be your first wind and solar power appliance.

- Create your own 100-calorie snacks Buy in bulk and divide it yourself. That packaging costs a lot and we pay for it in the end.

- Make drinks at home If you are going to have alcohol it is much cheaper do have drinks at home with friends than to do it at a bar.

- Clean dryer filters It helps you dryer work more efficiently and prevents fires.

- Clean refrigerator coils again it improve the efficiency of your fridge.

- Turn down the temperature on your water heater It can save a lot of money on energy. Unless you are like me and LOVE your HOT showers.

- Start a garden If you have any space it is a great rewarding experience. It takes some practice but you can grow your own food and it will be much better for you if you are doing it yourself.

- Start a compost pile Take your yard waste and kitchen scraps and start a compost pile or a worm bin and make your own Black Gold

- Reuse milk jugs You can use milk jugs with small holes in the bottom as a drip irrigation system.

- Don’t waste your water When you cook veggies with water, steam or boil. Use it to water your potted plants. The nutrients lost in the water will feed your plants. Just remember to let the water cool before you use it or it will kill your plants.

- Make your own cleaners Vinegar has tons of uses around the house and you can mix some up to clean and deodorize your home.

- Try a staycation If you stay home but disconnect from your normal routine you can get things done around the house or in your local area and save a lot of money.

- When possible go for energy saving appliances Save money in the long run with better energy ratings.

- Wear clothes more than once before washing when possible Unless if you are getting really dirty or are working really hard you can get away with more than one wear.

- Buy your own water filter Bottle your own water.

- Eat early or late when going out You can get early bird discounts or happy hours to save money.

- Keep your freezer full It takes more energy to keep an empty freezer cold.

{kind=link}

Kids

- Create a Babysitting Co-Op No not like those books from such a long time ago but if you and another couple can exchange babysitting services it will give both of you a free night out. This is great for your marriage as well as your wallet.

- Hand me arounds There is no reason to buy all new clothes for your child, especially when they can only where the same thing for a few months before they grow out of it. When you are done pass them along and find someone else to do the same with. My wife has a Mothers group at church that constantly passes clothes around and saves everyone a ton.

- Play at the Public Park Why not just go to the park and play with other kids, you already paid for it.

- Watch the local parks for educational programs Take your kids to these and they may have so much fun they won’t even realize they are learning.

- Public Libraries There is so much that can be had at public libraries from internet access to the books and learning programs.

- Use city services There are plenty of free (already paid for through taxes) activities for children around our city, between Metro parks and libraries there is plenty to keep them entertained.

- Watch local churches Especially in the summer there are tons of Vacations Bible Schools for kids’ activities.

- Stop spending so much on your kids Really they want your time and love more than anything. Make up games you can play at home all the time or just play tag.

Car

- Slow Down Aggressive driving and decrease your fuel efficiency by up to 33% according to the EPA.

- Driving the speed limit This also helps to save gas as gas mileage drops over 60 MPH.

- Empty your Trunk Getting excess weight out of your vehicle will give you better gas mileage.

- Change your oil Keep up with routine maintenance these jobs are not just to keep auto shops in business but they help your car drive better longer.

- Never buy new New cars are almost always a bad deal because of depreciation. Used cars will get you a much better bang for your buck

- Wash and vacuum your car at home There is no reason to pay for a vacuum and the automatic car washes don’t do the best job of your car.

- Wash it often Dirt can damage paint.

- Keep your tires inflated It will help you get better gas mileage; you also need to check them every few weeks.

- Use 2WD55 Air conditioning That is two windows down 55 MPH.

- Keep wheels aligned Your car is working hard if your alignment is off.

- Rotate your tires Prevent wear and make your tires last longer

- Find a way to carpool if possible I was able to carpool for over a year with a friend over a 40-minute commute, so it saved a lot of money.

- Leave the car behind Walk whenever possible, ride your bike if it is too far to walk.

- Move to just one car Can you do with only one car in your family, save on insurance, gas and maintenance?

- Look for discounts Ask your insurance company if you can get a discount for paying annually or with an automatic draft from your checking account.

Electronics

- Shop around. There are so many places to get a good deal online that you have to do your research.

- Buy Video games with replay value I have never been more disappointed than with THE video game that was supposed to be the be all end all of games and it took me 12 hours to finish. Some games you can play for hours some for days. Do the math 5/hr or .10/hr?

- Get books and DVDs from the Library Most libraries are stocked with DVD and unless it is a reference book you will need constantly you can get it for free at the library. If the library doesn’t have it, try sites like www.paperbackswap.com and www.dvdswap.com OR Find a friend who has it and borrow it. If you still can’t find it shop the used book stored then used on Amazon.com Then the retail store if you must.

- Think about an old fashioned solution? If people like Nelson Rockefeller can run multi-national corporations without a smart phone maybe we can too.

- Look into open source software Why pay for software when there are free and sometimes better solutions out there. http://www.osalt.com/ is a site dedicated to finding you the open source solutions you need.

- Check out Ting – Ting runs on the sprint network, if you don’t mind having an older phone for a while you can save a ton of money by switchting over to ting.

Banking

- Find the best interest rates around don’t just use the bank you always have. This isn’t 1950; banks don’t think of you as anything but a number (unless you have a very special bank) so don’t fall for their loyalty stuff. If they aren’t making the most of your money someone else will.

- Call your credit cards and ask for a better rate Although I had one bank drastically reduce my limit when I did this once when all the banks were tightening up. I paid off the card and haven’t done business with them since.

- Always use a reward Card. There are not as many as their used to be but they are still out there. Get paid if you can as long as you pay off the balance.

- Get an online savings account They tend to have higher interest rates than brick and mortar banks. I use and love Capital one 360

- Don’t overdraft your account it costs you too much money.

- Pay bills automatically Use bill pay from your bank to avoid late fees and save on postage.

- Keep your money in hard to reach places like an account you don’t have Internet access to. That way you are less inclined to spend it on a whim

- Freeze your credit cards Literally we have kept our cards in a tin can full of water in our freezer. If we need them we have them but we can’t just get them to spend carelessly. Especially when you can’t microwave it.

Shopping

- Sign up for rewards Programs I even set up a special email for them but you can get some good coupons and deals from a lot of these.

- Stick to the list A shopping list is not just there to remind you of what you need to buy but, it is also there to prevent you from buying things you don’t need.

- Drink more water Soft drinks at a restaurant can cost up to $3. If you drink water you will save a lot in the long run. Even at home it is cheaper.

- Buy more ingredients Prepares, processed, microwave meals are more expensive and less nutritious than buying the ingredients and making it yourself. We have seriously considered a “you can anything you want as long as you make it yourself rule)

- Buy and cook in bulk Wholesale clubs allow you to buy large amounts at a discount (although not always so keep an eye out). Store the food for later or prepare it all at once and then freeze it for use later.

- Constantly shop around on service like insurance Insurance policy rules are constantly changing you may be able to get a better rate from someone else check at least once a year.

- Check your deductibles you can save a great deal by increasing your deductibles, although make sure you have the money to cover your deductible in the event of an accident.

- Always ask for a discount The worst thing they can say is say “No” and it is easier every time you ask.

- Don’t be trendy Classic clothes last longer than trends. Besides you will most likely look back and realize how silly you looked

- Don’t buy dry clean only clothes You don’t want to spend the extra money

- Shop at outlets and stores like TJ Maxx “ You can often find better prices at these stores.

- Share a Meal If you are going to go out to eat try splitting a meal. Most casual dining restaurant meals are big enough to share and still be full.

- Buy a whole Chicken You can eat all of the meat and then boil the bones to make a stock.

- Get a larger prescription If you take a prescription medication on a regular basis, ask your doctor to write a three-month prescription. Instead of paying three co-pays, you only pay one.

- Use Baking soda for toothpaste It works just the same

- Plan meals that can be repurposed We make a pot roast and make open-faced sandwiches the next day out the leftover meat.

- If you eat out only do so when you have a coupon We decide where to eat based on the coupons we have in our collection.

- Don’t shop for groceries hungry You often end up buying so much more than you really wanted to.

- But generic when possible Store brands foods are much less expensive in most cases and the reduction on quality is not that noticeable except for Ketchup I have never found a generic ketchup that is as good Heinz.

- Watch for thrift store discount days Some stores have a 50% off day and you can get things on the cheap.

- Buy an Entertainment book It will cost you $20-30 but will save you a ton.

- Find out if an item has a price guarantee Some store will pay you back the difference if an item goes on sale shortly after you buy it.

- Always keep your receipts You will need them if you want to get your money back or need a repair

- Remember to send in your rebates Another reason to keep your receipts.

Other

- Adjust your tax allowances There is no reason to give Uncle Sam an interest free loan for the year while you are paying interest on your debt or while you could at least squeak a few dollars out of your savings account.

- Get the most out of your employer Make sure you are aware of all the benefits offered by your employer you can take advantage of. FSA, Tuition reimbursement, 401(K) match, adoptions assistance.

- Go to the second run or Dollar Theater Sure you won’t see it the day it comes out but Hollywood hasn’t been doing much worth the extra expense IMAO.

- Start or join a book club It is cheap and it great entertainment as well as being social with a real live person.

- Quit Smoking it isn’t getting any cheaper and it will save you money in the long run on medical expenses.

- Try grounding yourself for a period to reset your life style “ For a month stop watching TV or playing video games or whatever mindless thing sucks up your time. When the month is over you will find you didn’t need it much after all.

- Offer services instead of gifts A night of babysitting can be more valuable than gold.

What are your best money savers? Tell us below in the comments.

This article contains affiliate links that will pay for this site if you purchase anything through those links.

Gather your debt records

Your third step in the process is to gather your debt records. Student loans, credit card statements, car loan statement. Statements from all the debts you carry.

Putting all of this information in one place can be a little scary if you have never done the calculation before or are unsure of your current financial situation. The easiest way to conquer the fear of the unknown is to know it. Think of it this way, before your GPS will tell you which way to go it has to find your current location. This process is finding your current location so you can make the correct turns go forward.

There is information you need to know from each of your debt records

Balance

The total amount of money you owe on the debt.

Interest Rate

The cost of borrowing the money. This is usually listed as “interest rate” or “APR” which stands for Annual percentage rate.

Monthly Minimum Payment

How much you have to pay each month to not be delinquent on your debt. Keep in mind making minimum payments only it will take up to 20 years to pay off a credit card.

You can use this handy Google doc if you like.

All of this information will become very important as we move forward in getting rid of our debts.

Image by Kantamate555

Track your Spending

Track your spending

This is part two in a series on how to arrange your finances. If you haven’t already read part 1 to get off on the right track.

When you track your spending it will do a few things for you. It will help you determine where your money is really going each month. Many times we think we know how we are spending our money, but forget about little purchases we make along the way; nickle and diming your self, so to speak.

Secondly, you will actually spend your money more wisely. There is something about tracking spending that will make you think about purchases. It causes you to make more deliberate decisions when you are spending your money.

There are a couple of different ways to go about this. Feel free to use which ever one works for you. The importance is not in how you get it done but simply that you get it done.

I suggest signing up for mint.com or a similar service. This will import your records from your checking account and help you to categorize them appropriately. Although watch out, they are not always right, or the categories may be too broad.

Secondly, you can track your spending by hand. Keep receipts for everything you spend and write it all down. This way requires a bit more work on your end, but will help you more in controlling your spending, who wants to manually write down junk spending?

Once you have tracked your money for a month, you should have captured a majority of your spending and have a good idea of where you are starting from. It will make the following steps more easy and accurate.

Image by Ken Teegardin

Balance Giving vs Investing

When I get to the Q&A portion of my classes there is a question I always get. “How do you balance giving and saving/investing?”

I wish I had a straight answer for the question of giving vs investing, but any short answer does a disservice to the question itself. As believers we are called to give sacrificially and generously to those in need. And it is a part of our culture and even sensible to save money for things like retirement. If you are looking to build a retirement nest egg and give sacrificially it can be a struggle to find any balance between them.

Obviously this isn’t an easy question to answer but here are a few things to consider.

-

Are you living sacrificially?

Take a look at your budget and your spending and ask “Is my giving impacting my lifestyle?”

CS Lewis put it this way:

I am afraid the only safe rule is to give more than we can spare. In other words, if our expenditure on comforts luxuries, amusments etc is up to the standard common among those with the same income as our own we are probably giving away too little. If our chartities do not at all pinch or hamper us, I should say they are too small. There ought to be things we would like to do but can not because our charities exclude them (Mere Christianity)

-

Retirement isn’t biblical

This is a concept most people don’t realize. Retirement isn’t something the bible even addresses. Retirement is a twentieth century invention and it was created to force older workers out of the system so they would stop slowing down production. The only way to do it was to pay them not to work. Now it is just assumed that we will get to stop working one day even if we can’t afford it.

We may need to save for the loss of income as we reach retirement age, but shouldn’t assume that there will come a time where we are not working.

-

Giving in light of God

As Christians we should think about our giving in light of God as the great giver. God planned to show his goodness to us before the foundation of the world in giving his son to save us. Jesus models for us what type of sacrifice we are supposed to display.

Philippians says “Have this mind among yourselves, which is yours in Christ Jesus, who, though he was in the form of God, did not count equality with God a thing to be grasped, but emptied himself, by taking the form of a servant, being born in the likeness of men. And being found in human form, he humbled himself by becoming obedient to the point of death, even death on a cross.” Phil 2:5-8

If Jesus was willing to set aside equality with God we can be willing to set aside equality with our neighbors’ standard of living.

You should always have a car payment.

You should always have a car payment. Unless you live somewhere like NYC where you don’t need a car, then you can move on to another one of our great articles. You should always have a car payment, not so you can drive the newest model every year, that would be crazy. However, most of us are in a place where we will be needing a new car sooner or later. How are you going to pay for that car without going into debt and taking on a few hundred dollars a month?

Always have a car payment and make it to yourself.

If your car is paid off, find some money in your budget and dedicate it to your car fund. Even if it is just $50 or $100 dollars a month it will help a lot in the long run.

Think about it. If you take out a loan for a $10,000 car and you just pay the minimum you are paying around $2000 in interest over the course of the 5 year loan. That is 20% increase in the cost of the car. Would you have paid 20% more for your car up front?

Every thousand dollars you put down saves you close to $200 in extra interest. And perhaps you can even save enough to not need a loan in the first place. If you take good care of your car there is no reason why you can’t pay cash for your next one.

This habit also prevents lifestyle creep. If you always have a car payment you never get used to living without one. Then if you really did need to take out a loan you don’t won’t feel the squeeze in your budget, because the payment is already there.

I am a fan of driving a car as long as you can, but I will admit I don’t feel like taking that route with my wife and kids so perhaps she can get a newer car before I do.

Financial Samurai has a great article on how to determine how much you can spend on a car. It is an interesting idea but I am not sure how practical it is if you try to live it out. It would definitely help to prevent getting in over your head.

Prevent Fights About Money in Marriage

Photo by yourdon

I have talked to many couples about money over the years and there always seems to be some tension around money within marriages. According to some evidence fighting over money greatly increases chances of divorce. It may be a testament to how powerful the love of money is in our culture.

My wife and struggled with how to handle our finances in a biblical fashion and how to handle money issues within our marriage with the grace of the gospel and we have learned a few things about preventing fights about money in marriage:

- Don’t become money Pharisees: Many church folks talk about money with a very legalistic mindset. We set hard and fast rules to live by when it comes to our money and then we experience the same guilt with money that we do with every other sin in our lives because we broke the rules. You will both make mistakes or have already and there must be grace for those mistakes just like any other sins that have been forgiven by Jesus.

- Remember to communicate: It is easy if one spouse “Does the bills” or “Handles the money” for the other spouse to feel left out especially if that spouse also doesn’t bring in any income. I have had to work very carefully to keep my wife involved and help her to know that our money is OUR money. We have gone as far as to schedule a weekly finance meeting where we go over spending, budget and planning. Mint.com creates great little graphs for my presentations.

- Create and commit to your budget together: The initial budget should be something you and your spouse decide on together. It may be a tough conversation but you can help one another by calling out the idols you have in your life around money. My wife, by nature of taking care of our home, is responsible for spending a large share of our budget that isn’t automated. She does her best to stick to the budget we agree to and we discuss it when it needs to be changed.

- No questions asked money: If you can afford it allow one another play money. If my wife wants to order a new gadget for her camera she doesn’t have to ask me she just buys it. Similarly, I don’t have to ask her when I want to go out for lunch. We each have our own accounts with direct deposits that are ours alone.

- Automate things: When possible automate savings and bills. Saving is much less painless when you don’t have to do anything to accomplish it. We have a whole article on how to do it here.

- Ask “Why do I feel this way”: We all have experiences with money that lead us to think a certain way about it. I, for example, value my savings like an idol just for its own sake. I trust that having no debt and money in the bank will save me from life’s circumstances instead of trusting in Jesus as my savior.

- Know your Role: No not that men are the breadwinners and woman should be home barefoot and in the kitchen. (Although my wife hates shoes and loves to cook). Know how your individual styles complement one another. Or know what you can and cannot do. By way of example: My wife will hold onto cash like it is gold. She will spend that $50 in her purse several times. Each time intending to deposit it to cover the purchase she just made. I ,on the other hand, will hold onto cash and spend on a card because it isn’t concrete money to me.

This list, like most of this blog, is a monument to our failures. We have learned many of these lessons the hard way. What else can you do in order to prevent fights about money in marriage?

Automate Your Finances

One of the best steps in getting your budget under control is to automate finances. As much as possible, make your financial matters a hands off activity. This way you are eliminating human error like forgetting to send the payments or spending more than your budget allows, and your savings happens without your effort.

Limit access to money

One of the most effective ways to automate your finances and control your spending is to limit access to your money. Your money is going to be spent the question is if it will be spent where you would like. The best example of this is 401(k). This money is normally taken out of your paycheck before you see it, like taxes. So, you do not have a choice in how you spend that money. Most people never even pay attention to how much money is taken from them in taxes.

This can be done in very simple ways. If your company has a direct deposit option you can limit yourself by only depositing the amount you need for your budget into your main checking account while remaining funds should be deposited into a savings or investment account. This helps control lifestyle creep (the propensity to spend more as you make more) because you don’t actually see an increase in your main bank account where it can be easily spent.

Example:

If your monthly budget for your bills is $1000 and you get paid once per month you would only deposit $1000 into your main checking account. If your paycheck was $1200 then you would deposit $200 in a savings account.

If you got paid every two weeks you deposit $500 per check if you can balance your bills on two different pay periods, that may take some time to set up and get right.

This prevents you from having easy access to “extra money”. I use quotes there because all of your money should have a purpose even if it isn’t immediate, and there should be a plan for all of your money. Don’t let your money sit around and be lazy, send it off to work for you in an interest bearing account, or in an investment of some kind.

Automate your bills

Most utilities offer a budget program which allows you to pay the same amount all year round instead of being hit with high electric bills for your air conditioning in the summer and for your heating in the winter. They will average the last year of your bills and give you one median payment. This allows you to set up a recurring payments of a single amount; no forgetting and no sticker shock on your bills.

For years we split our bills in half and paid half every two weeks with our paychecks, to make sure we didn’t spend it while we were waiting for the bill. It forced us to do some manual work thanks to those three paycheck months but it wasn’t bad. Now we use a different account for monthly bills that doesn’t get touched so we always have enough money and the bills are set to pay the full amount automatically.

How have you automated your finances and made your life simpler?

- Automate your finances

Extra Income, what should I do?

To Pay or not to Pay (off your debt)

I get a form of this question all the time. Should I pay off debt or invest it? Paying off existing debt is a safe bet. Think of it this way, if you are paying 19% on a credit card then by paying off that card you are saving 19% interest. That is money in your pocket every month that you can use to pay off other bills or start investing.

If you debt is low interest and/or tax deductible you may be better off by paying your monthly minimums and investing the extra money you have. Here is why..

Using debt to make money

Imagine if I told you that I would pay you 100$ tomorrow if you loaned me 90$ today? Suppose that you didn’t have 90$, but you could borrow it from a friend and pay him back 95$ next week. You would make 5$. You can do the same thing with your debt if you have a solid investment plan and some time.

According to most resources, the average return from the stock market over the long term is between 7% and 12%. If you are paying 4% on your mortgage, for example, you could take extra money and pay off that debt or you could take the same extra money and invest it. Sure, you would be paying interest on that money, but over time you will make more money investing. There would be some months where you may not, if the stock market has a bad run, but over time you should make more money.

This type of decision is not to be entered into lightly. Previous performance is no indication of future performance. That means that the stock market could make 1% over the next 30 years and you would lose money.

Additionally, it may be more important for you to be out of debt and play things safe. You may want to leave the rat race and start your own business. This is why I normally tell people to pay off their debt. It is the right emotional choice for most people, but it is possible to make more money and possibly pay off your debt sooner with the proper investment strategy.

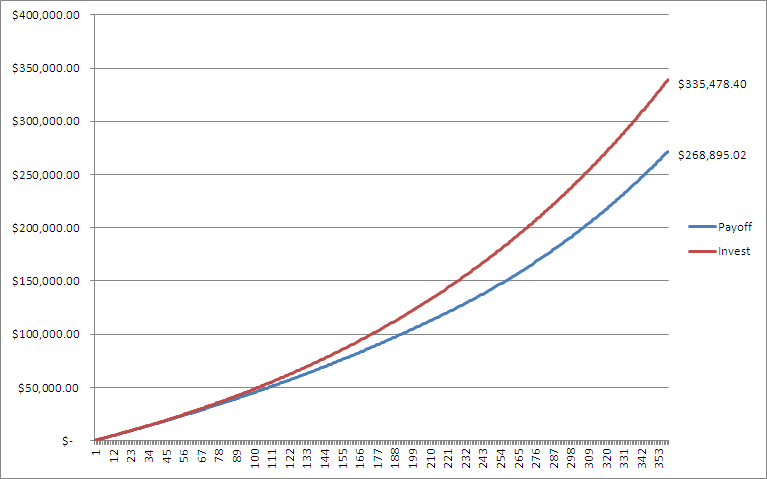

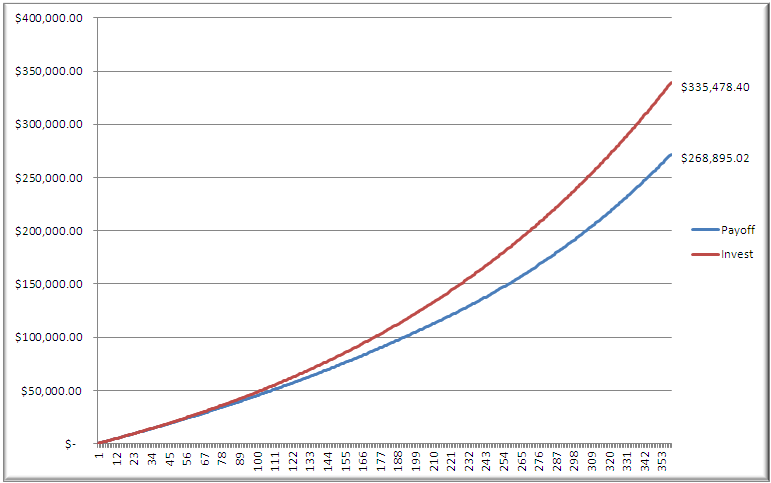

The chart below shows the difference in total value over 30 years when you invest at a conservative 6.5% instead of paying off a mortgage that has a rate of 3.5%. The numbers include the equity in the home as well as investment income. Once the mortgage is paid off the money that was being used to pay off the mortgage is then invested at 6.5%

Of course, there are many assumptions involved in these calculations. Your particular situation may be different, but many people have never even considered the benefits of not paying off their debt.

This is for informational purposes only, everyone should do their own investigation and due diligence.