Christian Stewardship Sermon

This is a sermon from Proverbs on Christian stewardship. Jason preached at the Veritas Tri-village congregation on 6/12/2016.

- Christian stewardship begins with understanding that God is the owner of everything (Ps 24:1). Christians understand that we are bought with a price and that it is God who gives us the power to gain wealth (Deut 8:18).

- Christian Stewardship is a spiritual discipline which can be exercised to produce godliness in the life of a Christian (1Tim 4:7)

- A good Christian steward, one who honors the Lord with their wealth.

- Worships with their offering

- Sacrifices with their giving

- Is Generous

- A cheerful giver

- Trusts the Lord will provide

- Plans and is intentional

- Stewardship is a Gospel issue

Podcast: Play in new window | Download

Why you and your spouse should have the money talk.

Recently, my wife and I have been slacking off on our money talk. I am the money nerd in our family so I track most of the data and I wanted to get back on track with keeping her in the loop.

1. The money talk keeps you accountable

It is easy to get sloppy with money. I am guilty of using more money than I should to by special treats for my family. Having a consistent money talk with my wife keeps me accountable. I know I will have to talk to her about those little treats. It makes me think twice and helps to keep us directed toward our goals. It isn’t that I am hiding bad things but those little treats are working against our goals.

2. The money talk keeps you on the same page.

It is easy to put the budget on cruise control. But, things can get out of line easily. Having the money talk will make sure you and your spouse are on the same page. It makes sure that the goals you set at one time are still the goals want to be pursuing. It gives you the opportunity to review and change those goals should the need arise.

3. The money talk brings you together.

This one was a big one for us most recently. I felt like I had let my family down by making some minor mistakes with the budget. We have a pretty complicated system and it is hard to manage sometime. Having the money talk was hard for me because it required me to admit I had made the mistakes and seek my wife’s forgiveness. It was tough on my pride, but it brought us together as a couple

Bottom line the more you talk about money the smoother it will go if you both are walking in grace.

Do you have any tips on how to have this conversation?

Image by kabaldesch0

How money minded people are throwing money away

If you follow many bloggers advice you are throwing money away without even realizing they are doing it. Personal finance writers talk a lot about delayed gratification. That’s the ability to put off things that you want now for better things later. We tell you to save up for the things you want instead of putting it on a credit card because it will cost you less and it is better to not be in debt. Every personal finance writer worth their keyboard can tell you about the Marshmallow Test and how it shows a child’s ability to delay reward and how it links to later success.

But here’s the thing, if you are delaying rewards just for later earthly rewards like a better retirement account then you are still throwing money away. Here is what Jesus had to say about it:

“Do not lay up for yourselves treasures on earth, where moth and rust destroy and where thieves break in and steal, but lay up for yourselves treasures in heaven, where neither moth nor rust destroys and where thieves do not break in and steal. For where your treasure is, there your heart will be also. (Matthew 6:19-21 ESV)

Often times when we are thinking about money we only get as far as this world. Saving for college, saving for an early retirement, saving for the new car or to get out of debt are all very good goals, but they are not the ultimate goals if you are a Christian. And far too often the people who are thinking about their money and being good stewards are still far to short sighted. If your 401(k) and your bank accounts and you houses look just like those of the people who are making the same amount of money as you then you are surely throwing money away where moth and rust may corrupt. Or worse yet you are heading down a path that Paul warns us is incredibly dangerous.

But those who desire to be rich fall into temptation, into a snare, into many senseless and harmful desires that plunge people into ruin and destruction. For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs. (1 Timothy 6:9-10 ESV)

Loving after money and desiring it can lead you to wander from the faith. We need to be aware of our own sinfulness and if we are one of these people who for whom money may cause our ruin, we should give it away all the more.

Ask yourself today, am I being selfish with my money? Am I giving sacrificially as the Bible calls me to do? Am I trusting God to provide or am I trusting in my savings account? If you aren’t sure of the answers, ask your spouse or a brother or sister who will be honest with you.

Original Image by Tax Credits

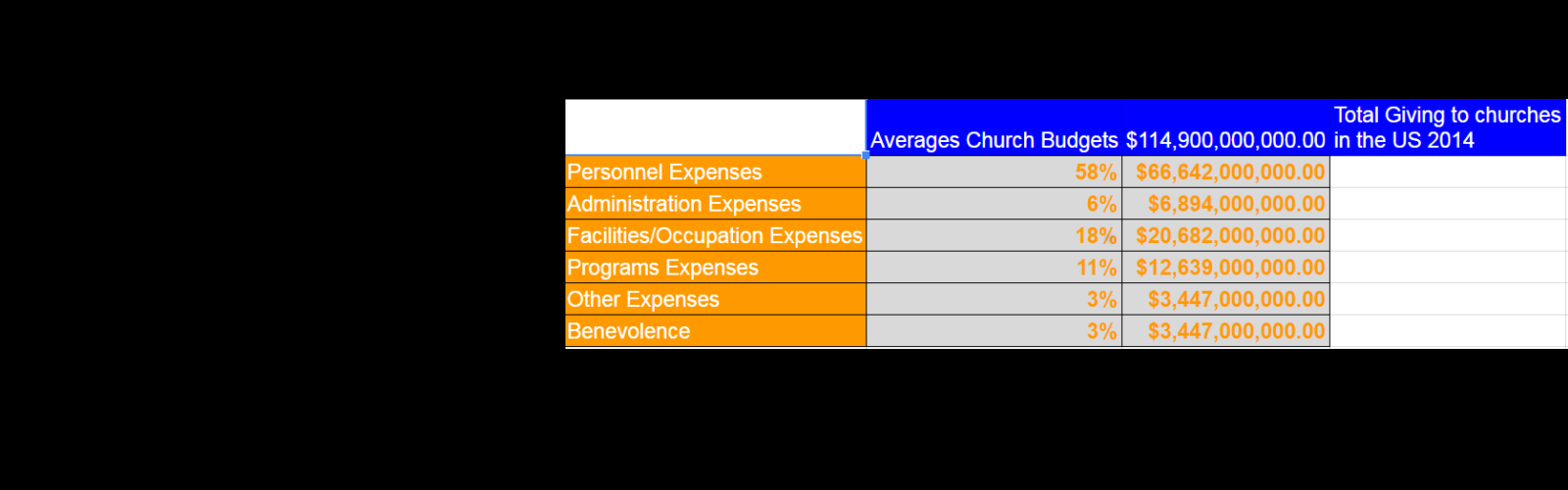

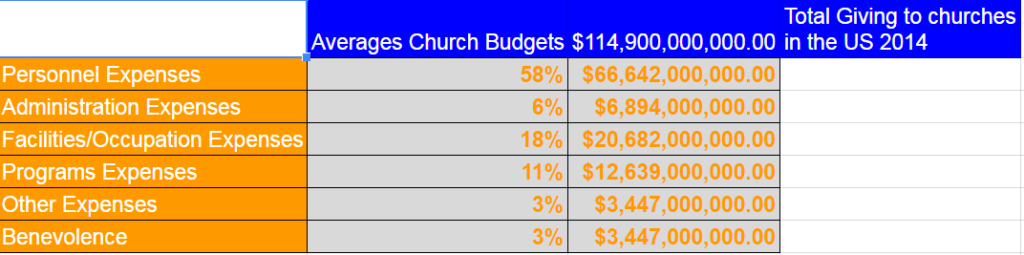

Church Budgets

This headline grabbed my attention…According to this article from Christianity Today, quoting a report from the Giving USA Foundation, American churches collected 114.9 BILLION dollars in 2014. (Numbers not available for 2015). We look at how church budgets break down on average. As we have discussed here before most of that money goes to keep the lights on and supply for the internal structure of the churches, as opposed to benevolence giving. (giving to those in need). If the popularity of Bernie Sanders has taught us anything it is that young people are more interested in our collective monies being used to help individuals and not to perpetuate the status quo, although they don’t care that said money is taken by force.

Let’s use the number collected by the Evangelical Credit union on church budgets to determine approximately how much of that money is being spent on what:

These numbers are an average simplification therefore the number to not equal 100%.

From Evangelical Credit union

Breaking these numbers down a bit we see some interesting things.

Personnel

This includes salaries, both full and part time, pension plan contribution, other benefits and taxes paid on behalf of employees.

Administration

Office supplies, postage, travel and membership dues.

Facilities

Utilities, maintenance and upkeep, debt (Mortgage) any other debt or fees associated with the building.

Program expenses

Children and youth programs, Adult programs, evangelism and outreach efforts, (benevolence has been pulled out to its own category)

Other Expenses

Building fund and cash reserves

Benevolence

Both local and international.

The numbers seem a bit off to me, even if you allow for program expenses to be outreach a full 82% of church budgets are paying salaries, building and to keep the lights on. Spending that is is some way inward facing. That is 94 BILLION dollars being spent by churches in the US to pay their pastors, buy their buildings and run their organizations. Charitywatch.org would give us a failing rating.

Of course, Charitywatch isn’t a fair comparison because pastors and staff are not strictly overhead, they are actually doing the work of the ministry in many cases. If we assume that half of the Pastors’ salaries are not overhead, but ends of our giving then our numbers are a little better at 53%. I am not sure of the best solution here, but I have been bothered by that 82% number ever since I read it. It feels like that money is more like paying country club dues that it is advancing the work of the Kingdom of God.

This is one of the primary reasons I have been attracted to the house church or cell church models over the years, it feels like a more efficient use of our collective resources. That being said I am part of a traditional model that thinks about this regularly and doesn’t actually fit these numbers for various reasons.

What do you think about these numbers?

Free Home Phone with Google Hangouts

With our kids getting older we felt we needed a home phone. Being who I am I wanted a free home phone. We don’t want a landline , but we don’t want to buy cell phones for our kids either.

We thought about adding another line to our Ting.com plan. That would only cost us $6 a month plus usage. Then I realized I could get a free home phone.

Self-Paced Email Course

If you are looking to get your budget under control our self paced course will help you every step of the way.

Sign up below to get each lesson in your mailbox as you complete the previous lesson.

Can I use reward cards?

One of the questions I get almost every time I speak on stewardship is around the use of reward cards. You know, the ones where they give you rewards points or cash back for spending money through them. As a general rule I am against consumer debt, credit cards, car loans and the like, but there is always someone who asks me about using cards for the cash back or for the rewards. They feel they can game the system somehow and make the banks pay.

My answer is as straight…absolutely depends. There are some folks who are diligent enough to pay off the card every month without fail. Those folks will make money from reward cards in the long run, but it doesn’t take much to ruin that streak and cost you all your winnings. Just like Vegas the house always wins.

A study of how rewards cards affect behavior in 2010 found that even a reward as small as 1% can change consumer behavior:

…consumers generally spend more and increase their debt when offered one percent cash-back rewards. The impact of a relatively small reward generates large spending and debt accumulation. On average, each cardholder receives $25 in cash-back rewards during our sample period. We find that average spending increases by $68 per month and average debt increases by over $115 per month in the first quarter after the cash-back reward program starts.

We all assume we are the exception to the rule, but that is not often the case. Banks spend millions of dollars to analyze the results of the incentives they give. That is why make the profits that they do.

I am not that person. I can do things if they are automatic. We use a reward card to funnel a few bills through that I automatically pay, but if I use it for anything else I end up paying interest even though I have the money to pay it off. I just like having the money in the bank more than not paying interest even though I know it is the wrong thing to do.

However, if you pay off your bill every month without fail you can make a little extra money with a reward card. It may just be best to ignore the fact that it is a reward cad and not try to game the system or you may find that you are the one being played.

4 Sinking Funds You Need

A sinking fund is simply saving up in advance for expenses that are inevitable. Often times we ignore upcoming expenses lead ourselves into a emergency. So, here are some sinking funds you need to think about.

1. Gifts – if you know anyone who is getting married anytime soon. If you celebrate Christmas or many other holidays you will need to buy gifts at some point. We like to keep a “Christmas” account funded with direct deposits throughout the year. We pull from it whenever we need to purchase a gift for any reason, but we use it mostly at the end of the year for Holiday spending and travel. It helps save our budget at the end of the year.

2. New Car – Your car is dying. Let’s face it. You are eventually going to need a new car. We have published another article on this topic specifically. You should always have a car payment. If you save up money as you are driving your current car into the ground you may have enough to pay cash or at least have a good down payment for your next car when you current one dies.

3. Phones – Our most cherished possessions and the bane of our existence when things go wrong. If you are like me every two years you want a new phone. I listen to a lot of tech podcasts and they are always talking about new phones. I also use ting.com so I have to pay off contract price for my phones, but pay much less for my service. If you like tech toys start putting money away not because your phone is dying faster than your car.

4. House Repairs – If you like it or not, you are going to need money to keep your home up and running. You should have an emergency fund for small things, but what about a new roof, or remodeling your house or larger items. You may need to repave the driveway or have a pipe burst in the laundry room. You could use your emergency fund for this, but that isn’t exactly what it is for. If you know it is coming it isn’t an emergency, it may just be something you didn’t plan for.

What are other sinking funds you plan for?

Image by Reinhard Jahn (Own work) [GFDL (http://www.gnu.org/copyleft/fdl.html) or CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

100 Money Saving Tips

Here are 100 money saving tips you can use to pay off your debt, give or save to invest. If you like it please share on your favorite social network.

- Adjust the Thermostat In the summer turn it up and in the winter turn it down. You will use less energy. Get a programmable thermostat if your house is empty during the day; you can save a lot of money and still have the temperature you want in your house before you get home.

By Jess from Canada (HPIM4771) [CC-BY-SA-2.0], via Wikimedia Commons

- Cut the cable Cable TV is becoming increasingly expensive as well as increasingly redundant since most networks are putting their content online, either on their own websites or on sites like HULU.

- Combine it if you can’t cut the cord then at least find out if you can bundle the services and save money in the process.

- Threaten to cancel and see what kind of deal you can get; Cable companies are striving for subscriber numbers right now and just want to hold onto their current clients. You can get a greatly reduced rate if you just tell them you want to cancel.

- Entertain at home A game night or a nice dinner is much cheaper and nicer in many cases, when done at home. Find other like-minded people and find creative activities.

- Learn how to sew a button Don’t throw away clothes because of minor issues. Sew the button back on if you stain your jeans or rip them make them your yard work jeans.

- Make gifts don’t buy them Making quality gifts takes time, but the person getting the gift may appreciate it much more.

- Convert to a gas or an instant water heater They are more efficient and can save a lot of money over time.

- Replace incandescent bulbs with CFL although there is some debate on this you can test and see if it helps you save money.

- Get rid of your home phone With cell phones being what they are now there is very little reason to have a land line. If you don’t get the best service at your home many cell phone providers will give you a device that will boost the signal in your home. It is like having a tower in your house.

- Shut vents in unused rooms This may not be a good idea if you have forced air heating, but shutting vents in unused rooms can save on your heating and cooling bill.

- Change the filters in your home every 6 months This makes your HVAC work more efficiently

- Use a power strip to turn off your entertainment system There is a term being used call vampire power where a lot of new electronics draw small amounts of power even when they are turned off. Using a power strip can eliminate that power draw and save you money.

- Buy used when possible Pay extra for a used quality product instead of a disposable quality product. Especially when it comes to kids items that they will outgrow in 6 months.

- Get live in help If you have a spare room you can rent it out to someone you trust.

- Pay your mortgage on a bi-weekly schedule Doing this can shave years and thousands of dollars from your mortgage.

- Clean your own carpets You can rent the machine or borrow it from someone.

- Attend College online It is much cheaper to get your education online just do your research and find a good school. I just finished my degree in 2.5 years.

- Delay purchases When you have a desire to purchase something wait a few days maybe even 30 to make sure you still want to spend the money on it.

- Buy a Clothes line Running a dryer costs a lot of money. This can be your first wind and solar power appliance.

- Create your own 100-calorie snacks Buy in bulk and divide it yourself. That packaging costs a lot and we pay for it in the end.

- Make drinks at home If you are going to have alcohol it is much cheaper do have drinks at home with friends than to do it at a bar.

- Clean dryer filters It helps you dryer work more efficiently and prevents fires.

- Clean refrigerator coils again it improve the efficiency of your fridge.

- Turn down the temperature on your water heater It can save a lot of money on energy. Unless you are like me and LOVE your HOT showers.

- Start a garden If you have any space it is a great rewarding experience. It takes some practice but you can grow your own food and it will be much better for you if you are doing it yourself.

- Start a compost pile Take your yard waste and kitchen scraps and start a compost pile or a worm bin and make your own Black Gold

- Reuse milk jugs You can use milk jugs with small holes in the bottom as a drip irrigation system.

- Don’t waste your water When you cook veggies with water, steam or boil. Use it to water your potted plants. The nutrients lost in the water will feed your plants. Just remember to let the water cool before you use it or it will kill your plants.

- Make your own cleaners Vinegar has tons of uses around the house and you can mix some up to clean and deodorize your home.

- Try a staycation If you stay home but disconnect from your normal routine you can get things done around the house or in your local area and save a lot of money.

- When possible go for energy saving appliances Save money in the long run with better energy ratings.

- Wear clothes more than once before washing when possible Unless if you are getting really dirty or are working really hard you can get away with more than one wear.

- Buy your own water filter Bottle your own water.

- Eat early or late when going out You can get early bird discounts or happy hours to save money.

- Keep your freezer full It takes more energy to keep an empty freezer cold.

{kind=link}

Kids

- Create a Babysitting Co-Op No not like those books from such a long time ago but if you and another couple can exchange babysitting services it will give both of you a free night out. This is great for your marriage as well as your wallet.

- Hand me arounds There is no reason to buy all new clothes for your child, especially when they can only where the same thing for a few months before they grow out of it. When you are done pass them along and find someone else to do the same with. My wife has a Mothers group at church that constantly passes clothes around and saves everyone a ton.

- Play at the Public Park Why not just go to the park and play with other kids, you already paid for it.

- Watch the local parks for educational programs Take your kids to these and they may have so much fun they won’t even realize they are learning.

- Public Libraries There is so much that can be had at public libraries from internet access to the books and learning programs.

- Use city services There are plenty of free (already paid for through taxes) activities for children around our city, between Metro parks and libraries there is plenty to keep them entertained.

- Watch local churches Especially in the summer there are tons of Vacations Bible Schools for kids’ activities.

- Stop spending so much on your kids Really they want your time and love more than anything. Make up games you can play at home all the time or just play tag.

Car

- Slow Down Aggressive driving and decrease your fuel efficiency by up to 33% according to the EPA.

- Driving the speed limit This also helps to save gas as gas mileage drops over 60 MPH.

- Empty your Trunk Getting excess weight out of your vehicle will give you better gas mileage.

- Change your oil Keep up with routine maintenance these jobs are not just to keep auto shops in business but they help your car drive better longer.

- Never buy new New cars are almost always a bad deal because of depreciation. Used cars will get you a much better bang for your buck

- Wash and vacuum your car at home There is no reason to pay for a vacuum and the automatic car washes don’t do the best job of your car.

- Wash it often Dirt can damage paint.

- Keep your tires inflated It will help you get better gas mileage; you also need to check them every few weeks.

- Use 2WD55 Air conditioning That is two windows down 55 MPH.

- Keep wheels aligned Your car is working hard if your alignment is off.

- Rotate your tires Prevent wear and make your tires last longer

- Find a way to carpool if possible I was able to carpool for over a year with a friend over a 40-minute commute, so it saved a lot of money.

- Leave the car behind Walk whenever possible, ride your bike if it is too far to walk.

- Move to just one car Can you do with only one car in your family, save on insurance, gas and maintenance?

- Look for discounts Ask your insurance company if you can get a discount for paying annually or with an automatic draft from your checking account.

Electronics

- Shop around. There are so many places to get a good deal online that you have to do your research.

- Buy Video games with replay value I have never been more disappointed than with THE video game that was supposed to be the be all end all of games and it took me 12 hours to finish. Some games you can play for hours some for days. Do the math 5/hr or .10/hr?

- Get books and DVDs from the Library Most libraries are stocked with DVD and unless it is a reference book you will need constantly you can get it for free at the library. If the library doesn’t have it, try sites like www.paperbackswap.com and www.dvdswap.com OR Find a friend who has it and borrow it. If you still can’t find it shop the used book stored then used on Amazon.com Then the retail store if you must.

- Think about an old fashioned solution? If people like Nelson Rockefeller can run multi-national corporations without a smart phone maybe we can too.

- Look into open source software Why pay for software when there are free and sometimes better solutions out there. http://www.osalt.com/ is a site dedicated to finding you the open source solutions you need.

- Check out Ting – Ting runs on the sprint network, if you don’t mind having an older phone for a while you can save a ton of money by switchting over to ting.

Banking

- Find the best interest rates around don’t just use the bank you always have. This isn’t 1950; banks don’t think of you as anything but a number (unless you have a very special bank) so don’t fall for their loyalty stuff. If they aren’t making the most of your money someone else will.

- Call your credit cards and ask for a better rate Although I had one bank drastically reduce my limit when I did this once when all the banks were tightening up. I paid off the card and haven’t done business with them since.

- Always use a reward Card. There are not as many as their used to be but they are still out there. Get paid if you can as long as you pay off the balance.

- Get an online savings account They tend to have higher interest rates than brick and mortar banks. I use and love Capital one 360

- Don’t overdraft your account it costs you too much money.

- Pay bills automatically Use bill pay from your bank to avoid late fees and save on postage.

- Keep your money in hard to reach places like an account you don’t have Internet access to. That way you are less inclined to spend it on a whim

- Freeze your credit cards Literally we have kept our cards in a tin can full of water in our freezer. If we need them we have them but we can’t just get them to spend carelessly. Especially when you can’t microwave it.

Shopping

- Sign up for rewards Programs I even set up a special email for them but you can get some good coupons and deals from a lot of these.

- Stick to the list A shopping list is not just there to remind you of what you need to buy but, it is also there to prevent you from buying things you don’t need.

- Drink more water Soft drinks at a restaurant can cost up to $3. If you drink water you will save a lot in the long run. Even at home it is cheaper.

- Buy more ingredients Prepares, processed, microwave meals are more expensive and less nutritious than buying the ingredients and making it yourself. We have seriously considered a “you can anything you want as long as you make it yourself rule)

- Buy and cook in bulk Wholesale clubs allow you to buy large amounts at a discount (although not always so keep an eye out). Store the food for later or prepare it all at once and then freeze it for use later.

- Constantly shop around on service like insurance Insurance policy rules are constantly changing you may be able to get a better rate from someone else check at least once a year.

- Check your deductibles you can save a great deal by increasing your deductibles, although make sure you have the money to cover your deductible in the event of an accident.

- Always ask for a discount The worst thing they can say is say “No” and it is easier every time you ask.

- Don’t be trendy Classic clothes last longer than trends. Besides you will most likely look back and realize how silly you looked

- Don’t buy dry clean only clothes You don’t want to spend the extra money

- Shop at outlets and stores like TJ Maxx “ You can often find better prices at these stores.

- Share a Meal If you are going to go out to eat try splitting a meal. Most casual dining restaurant meals are big enough to share and still be full.

- Buy a whole Chicken You can eat all of the meat and then boil the bones to make a stock.

- Get a larger prescription If you take a prescription medication on a regular basis, ask your doctor to write a three-month prescription. Instead of paying three co-pays, you only pay one.

- Use Baking soda for toothpaste It works just the same

- Plan meals that can be repurposed We make a pot roast and make open-faced sandwiches the next day out the leftover meat.

- If you eat out only do so when you have a coupon We decide where to eat based on the coupons we have in our collection.

- Don’t shop for groceries hungry You often end up buying so much more than you really wanted to.

- But generic when possible Store brands foods are much less expensive in most cases and the reduction on quality is not that noticeable except for Ketchup I have never found a generic ketchup that is as good Heinz.

- Watch for thrift store discount days Some stores have a 50% off day and you can get things on the cheap.

- Buy an Entertainment book It will cost you $20-30 but will save you a ton.

- Find out if an item has a price guarantee Some store will pay you back the difference if an item goes on sale shortly after you buy it.

- Always keep your receipts You will need them if you want to get your money back or need a repair

- Remember to send in your rebates Another reason to keep your receipts.

Other

- Adjust your tax allowances There is no reason to give Uncle Sam an interest free loan for the year while you are paying interest on your debt or while you could at least squeak a few dollars out of your savings account.

- Get the most out of your employer Make sure you are aware of all the benefits offered by your employer you can take advantage of. FSA, Tuition reimbursement, 401(K) match, adoptions assistance.

- Go to the second run or Dollar Theater Sure you won’t see it the day it comes out but Hollywood hasn’t been doing much worth the extra expense IMAO.

- Start or join a book club It is cheap and it great entertainment as well as being social with a real live person.

- Quit Smoking it isn’t getting any cheaper and it will save you money in the long run on medical expenses.

- Try grounding yourself for a period to reset your life style “ For a month stop watching TV or playing video games or whatever mindless thing sucks up your time. When the month is over you will find you didn’t need it much after all.

- Offer services instead of gifts A night of babysitting can be more valuable than gold.

What are your best money savers? Tell us below in the comments.

This article contains affiliate links that will pay for this site if you purchase anything through those links.

Dave Ramsey – My first impression

I have been writing on personal finance and helping people with their money for years, but I have avoided Dave Ramsey like a OSU fan avoids maize and gold. I didn’t want to be overtly influenced by what some people consider the definitive author of personal finance. I realize, of course, that since most of what is taught in the PF world is common sense it all seems derivative, but I still prefer to feel like I am not copying someone else’s work.

been writing on personal finance and helping people with their money for years, but I have avoided Dave Ramsey like a OSU fan avoids maize and gold. I didn’t want to be overtly influenced by what some people consider the definitive author of personal finance. I realize, of course, that since most of what is taught in the PF world is common sense it all seems derivative, but I still prefer to feel like I am not copying someone else’s work.

Dave Ramsey is an Evangelical Christian who makes his name by teaching people “God’s way to handle their money”. I have been asked to assist with facilitating Dave Ramsey’s Financial Peace University, his magnum opus, and so I held my breath and plunged in. It wasn’t as bad as I thought it might be on many levels. Dave is a very polished presenter with a delivery that reminds me of comedian Bill Engvall (they also have the same eyes) his use of humor was engaging and kept me from becoming completely bored, I can’t stand to be on the receiving end of a monologue.

Having said all of that, I am troubled that some of the things he says abuse the bible to prove his way is God’s way. He uses the bible to proof text his points, but has yet to address any passages that would contrast his “God wants you to have the American dream message.” For example, Jesus call in Luke 14:33 “So therefore, any one of you who does not renounce all that he has cannot be my disciple.” Or the fact that the Bible has very little good to say about money unless it is being given away. As a recovering member of the prosperity gospel movement this makes me very nervous.

We are only three weeks into the class so I hope I my mind will be changed as I move forward but I wanted to get my first impression out there before it is too late.

Have you ever taken the course? Tell me if it gets better in the comments below.

Photo courtesy of Jessica Adkins