New Year Budget Recap

You have determined your goals.

You have Tracked your Spending.

Determined how to actually make payments on your debt and pay it off.

NOW WHAT?

This part sucks. While it is definitely not a set it and forget it situation there may not be any big moves for a while. Now you are in the phase where you simply do what you know you need to do. That is not very exciting until you hit a milestone like paying something off. It is OK to set little rewards for your self when you pay off your first debt or give that extra charitable gift. These are awesome things and you should celebrate. If you are good with excel you can plot out what you will be doing a year or five years from now and that can give you something to look forward to in a big way.

Look back to the goals you set out in the beginning of this course. They will encourage you to push on when you don’t feel like you can go on any further. Find folks that can encourage you to keep pushing on in the right direction.

Keep a close watch on your budget and your plan early on and make sure you are going in the right direction. Find extra ways to make money, I will be talking about those shortly.

Send me any questions if you need help @thinksteward. #newyearbudget

image by TheBo

Revisit your Budget

Revisit your Budget

Budgets are living, breathing, documents. They will need to change as your lifestyle changes. These changes need to be done intentionally and not accidentally. How do you do this with your budget?

Budgets are living, breathing, documents. They will need to change as your lifestyle changes. These changes need to be done intentionally and not accidentally. How do you do this with your budget?

Pay attention to it for starters. The biggest mistake people make is to ignore the budget they have just put together. It is easy to assume that everything will take care of itself now that your monster spread sheet is put together or that you have set everything up on mint.com. But, alas, it simply isn’t that easy.

I will let you in on something, even if you used my budget template as I suggested, you forgot something on your budget. There is a bill that will come due that wasn’t part of your initial tracking period. That is OK. You will just need to adjust your budget now. Is it ok to change your budget? If it is intentional, absolutely. Budgets change, the problem arise when you simply overspend, without planning. You will need to adjust your budget several times until you have it to a good place and then you will, hopefully, get a raise or something else will change in your financial life that will require you to change or even rewrite your budget.

Understanding that your budget is a living document will help you not stress out when things come up that you require you to make adjustments.

- What could I have forgotten?

- Did you put money aside for the Holidays? That is one of the biggest times to destroy your budget. Save money for travel, gifts and extra workout equipment to get rid of those holiday meals meals.

- Bills that don’t come due every month; Car insurance, homeowners insurance; subscription fees.

- Do you have an emergency fund? Cars need repairs, hot water tanks blow up. If you don’t want to blow your budget you need to have money put aside for these things, they will happen.

- It also helps to give yourself an allowance so you have some money to spend when you want something. Leaving yourself out of the budget will lead to burnout.

- What else can you do to improve your budget?

You will need to make changes to your budget, it is inevitable. Make them carefully and deliberately, not during emotionally charged moments. Don’t sweat it, life changes, change with it.

Image by lendingmemo

Create your debt snowball

Create your debt snowball

Create your debt snowball

Now that you have created a little wiggle room in your budget you can start making a move to get your debt paid off. We are going to use a popular method among personal finance writers, including Dave Ramsey. It is called the debt snowball because as you pay off debt you use the former payment for that debt to pay off your next debt gaining momentum as you roll down your freedom mountain.

Let’s look back at your debt records and set up your snowball. First you need to prioritize your debts in the order you will pay them off. There are two main schools of thought on this issue. Do you pay them off in the order that gives you a better emotional advantage or the better mathematical advantage.

If you pay off your highest interest rate debts first, mathematically you will pay less in interest, but it may be a long time until you clear that hurdle of paying off your first debt. If you pay off your smallest debt first you will get the emotional push of success but you will pay more in interest in the long run. Neither of these is the absolute right way. After all, if you are going to fail without the emotional push it doesn’t matter how much more money you can save by doing it the other way. Decide which way works best for you.

If you are a numbers nerd, like me, or just want to see a visual representation of how the snowball works then take a look at the template over at Vertex42. I was going to create my own but theirs is everything I would have wanted to create. They also have video instructions to help you along the way.

Continue to pay all of your minimum payments on all of your debts. Take the extra money in your budget and put it toward paying off your debt. Then when that first debt is paid off take all of that money (the minimum and extra) and apply it to the next payment. Given enough time you will pay off your debt.

Image by BeverlyLR

Create Wiggle Room in your Budget

Creating wiggle room in your budget.

Creating wiggle room in your budget.

So you have just created your budget and you now you want to get started in paying off your debt, but you don’t think you have enough extra money to really make a difference. Well, this step is about finding ways to create some wiggle room in your budget. Doing this requires dedication and sacrifice.

Here are some ideas; your goal in this step is to try at least 5. The more effort you put into this step the faster it will be to pay off your debt.

1. Get more in your paycheck instead of in your refund. By using this IRS calculator you can find the real amount you should have withheld from your paycheck. Use the extra money to start paying off your debt.

2. Take the Chicken Challenge – The Chicken Challenge was coined by the Cord Killers Podcast. Call your cable company and tell them you want to cancel your cable. Worst case is you actually cancel it and live off netflix or hulu, more than likely they will cut your bill.

3. Take a look at your cell phone bill, look at other carriers like republic, or PCS wireless or any other smaller carriers that may give you a smaller bill each month.

4. Look over this list of 100+ ways to save money.

5. Get creative, if you are serious about getting your financial life under control then you may have to do things you have never done and make sacrifices you have never made to be successful.

6. Stop eating out for a month

7. Suspend any other subscriptions that are costing you money each month.

Image by svilen001

Gather your debt records

Your third step in the process is to gather your debt records. Student loans, credit card statements, car loan statement. Statements from all the debts you carry.

Putting all of this information in one place can be a little scary if you have never done the calculation before or are unsure of your current financial situation. The easiest way to conquer the fear of the unknown is to know it. Think of it this way, before your GPS will tell you which way to go it has to find your current location. This process is finding your current location so you can make the correct turns go forward.

There is information you need to know from each of your debt records

Balance

The total amount of money you owe on the debt.

Interest Rate

The cost of borrowing the money. This is usually listed as “interest rate” or “APR” which stands for Annual percentage rate.

Monthly Minimum Payment

How much you have to pay each month to not be delinquent on your debt. Keep in mind making minimum payments only it will take up to 20 years to pay off a credit card.

You can use this handy Google doc if you like.

All of this information will become very important as we move forward in getting rid of our debts.

Image by Kantamate555

Track your Spending

Track your spending

This is part two in a series on how to arrange your finances. If you haven’t already read part 1 to get off on the right track.

When you track your spending it will do a few things for you. It will help you determine where your money is really going each month. Many times we think we know how we are spending our money, but forget about little purchases we make along the way; nickle and diming your self, so to speak.

Secondly, you will actually spend your money more wisely. There is something about tracking spending that will make you think about purchases. It causes you to make more deliberate decisions when you are spending your money.

There are a couple of different ways to go about this. Feel free to use which ever one works for you. The importance is not in how you get it done but simply that you get it done.

I suggest signing up for mint.com or a similar service. This will import your records from your checking account and help you to categorize them appropriately. Although watch out, they are not always right, or the categories may be too broad.

Secondly, you can track your spending by hand. Keep receipts for everything you spend and write it all down. This way requires a bit more work on your end, but will help you more in controlling your spending, who wants to manually write down junk spending?

Once you have tracked your money for a month, you should have captured a majority of your spending and have a good idea of where you are starting from. It will make the following steps more easy and accurate.

Image by Ken Teegardin

New Year Goals

New Year Goals

First, let’s talk about why you are taking this course? Why do you want to get your finances under control and pay off debt. Having these reasons straight in your mind can help you succeed when the going gets tough.

These reasons are very important because they will need to be your motivation when things get tough. There will come a time in this journey when you are going to want to give up because things just aren’t fun and exciting anymore. Because things aren’t as easy as you thought they would be or when things aren’t moving as fast as you thought or when you hit a major setback.

Do you want more money when you retire?

Do you want more money when you retire?

Do you want be a better steward of the gifts God has given you?

Do you want to save up for your family?

Do you want to get out from under the crushing weight of debt so you can feel some freedom?

Do you want to get your finances under control

Seek out every reason you can, intellectual, scriptural, emotional and write full sentences about why you want to take this journey. Make these personal reasons that will mean something to you as you move through the process of getting debt under control.

Take your time on this step, it would be easy to cast it aside and just jot down a few things, but the more time you spend on your foundation the better off you will be down the line. You will refer to this down the road when you need motivation.

This is the first in a series designed to help you start the New Year off right. Make sure you don’t miss out on any pieces of the series subscribe to our site by email.

Image by BK

New year budget

It is time for a new year budget; A lot of folks choose to use the new year as a starting point to achieve goals they have put off all year. If your goal is to start being a better steward of your money, get out of debt and take control of your financial life then I have good news. Starting next week I am going to start publishing a course on how to do exactly that. It will include step by step instructions on how to do just that. You can follow the course on this site or subscribe to the email list below to ensure you don’t miss anything.

It is time for a new year budget; A lot of folks choose to use the new year as a starting point to achieve goals they have put off all year. If your goal is to start being a better steward of your money, get out of debt and take control of your financial life then I have good news. Starting next week I am going to start publishing a course on how to do exactly that. It will include step by step instructions on how to do just that. You can follow the course on this site or subscribe to the email list below to ensure you don’t miss anything.

The course will cover:

- Why you want to be a good steward of your money

- Setting your personal goals

- Creating a budget to help get you there

- Overcoming obstacles that WILL come up

- A lot more…

Sign up for our mailing list so you don’t miss a thing.

Image by sally_12

Looking for a new house

So, my wife and I have been looking into buying a new house. We have been living in our “starter home” for over 10 years now. We didn’t intend to be in it this long and with two growing girls we feel like we need to move on and get something a little larger. What are our considerations?

Are you creating an idol in our new house?

We think there is a distinct possibility that we may be looking for a house to provide peace that only God can provide. Although we do want to show more hospitality it is very easy for a new home to consume more of your life than it frees up. I have recently had a conversation with a friend who asked me if it was possible his house had become an idol of sorts. The question is why do we want a new home. We need some more space for our family including more in the ways of storage. We would like some more land in a more rural area partly so we can enjoy some peace and partly to enjoy activities that require more space, like archery and four-wheelers.

How much can we afford?

This is another big question. According to several calculators on the subject we can afford anywhere between 180 and 350k. Which is crazy! I couldn’t imagine making that kind of mortgage payment. We have a budget in place now that allows us to be fairly generous with out money while putting some away. Moving will mean we need to adjust out budget accordingly and we need to understand those changes. So the question is not “What can we afford?” but “How do we want to spend God’s money?”

Should we even move?

This is the question I really don’t want to ask myself. We have some great neighbors and our church has just planted a new congregation in our neighborhood. (after 5 years of driving 25 minutes to church). We could stay in our home and pay it off faster while keeping a lower mortgage payment and keeping more freedom in our budget.

Space is subjective I suppose, we feel cramped, but according to this article living space per person has doubled since 1973. Maybe our culture is just telling us that we need more space.

These are some of the questions that I will be reviewing over the next few months or until we make a decision…

Image by Jan Tik

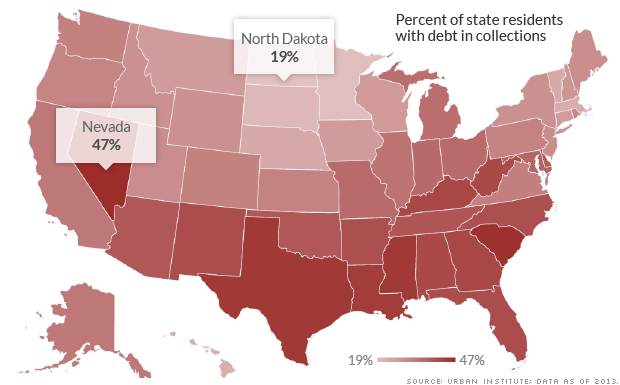

1 in 3 American adults have ‘debt in collections’

This is a pretty scary number. This is why being a good steward of your finances is so important.

Debt in collections by state

Americans have a debt problem. An estimated 1 in 3 adults with a credit history — or 77 million people — are so far behind on some of their debt payments that their account has been put “in collections.” That’s a key finding from a new Urban Institute study.

HT to: http://ift.tt/1nC2iSX