Is Pursuing Christian Wealth Worth the Spiritual Risk?

I read a lot of personal finance bloggers, many of them Christian. It seems to me that many of them ask “Can we?” in regard to Christian wealth, but rarely ask if we should. Dave Ramsey, for example, talks a lot about handling money God’s way. He says that God’s way will lead to having a lot of money that you can give away later after you are established. Very similar to the prosperity gospel I was a part of; the goal was always to get more money for the sake of God’s kingdom, but it would make us wealthy along the way.

There is no specific text in scripture that says the accumulation of wealth is a sin. However, there are enough warnings given concerning money and the love of it that we should ask if we should be pursuing wealth, at the same rate and with the same intensity as the rest of the world, is really worth it. For example:

Matthew 19 – After telling the rich young ruler to sell all that he has he turns to his disciples and says “Truly, I say to you, only with difficulty will a rich person enter the kingdom of heaven. 24 Again I tell you, it is easier for a camel to go through the eye of a needle than for a rich person to enter the kingdom of God.”

The disciples were astonished because they saw wealth as a direct sign of God’s blessing. If that person couldn’t enter the kingdom then who could? This is because money clouds our vision and prevents us from seeing our need for God’s grace. (And no there is no evidence of a small door called the “eye of the needle” that camels had to crawl through)

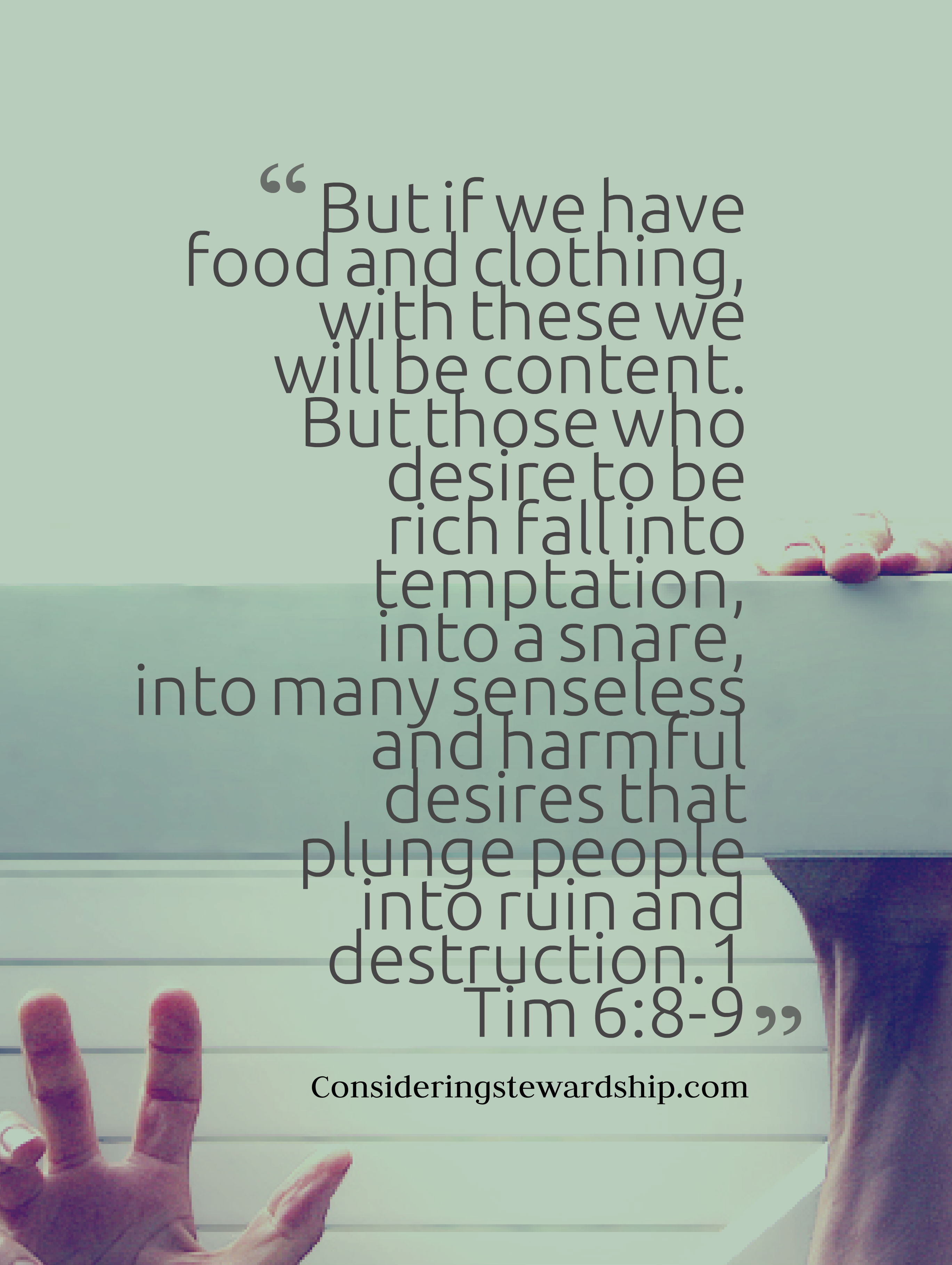

1 Tim –[6] But godliness with contentment is great gain, [7] for we brought nothing into the world, and we cannot take anything out of the world. [8] But if we have food and clothing, with these we will be content. [9] But those who desire to be rich fall into temptation, into a snare, into many senseless and harmful desires that plunge people into ruin and destruction. [10] For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs.

Paul calls to be content with food and clothing because of the inherent dangers in the pursuit of wealth. Of course, we don’t pursue money for it’s own sake. Of all the Christians pursuing wealth, not one of them would say it is for their own sake. Paul seems to be warning a Christian that no longer exists in our day. We only want money for the good it can do, but Paul didn’t seem to be to concerned about our good intentions. He seems to think the risk wasn’t worth the results. The very thing we pursue with such vigor can tempt and draw us to destruction. Is it worth the risk?

I know I am taking a hard stand and I would love to hear your comments below as I process this.

Image by jakerust

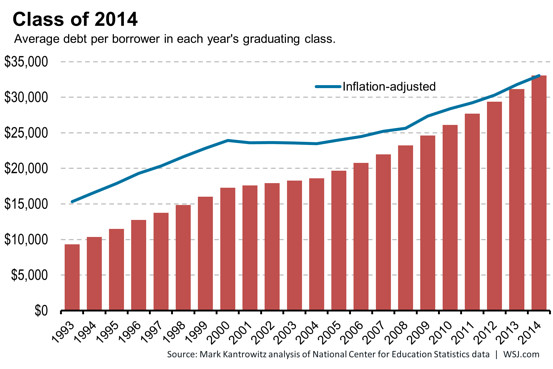

Congratulations to Class of 2014, Most Indebted Ever

The Wall Street Journal says “As college graduates in the Class of 2014 prepare to shift their tassels and accept their diplomas, they leave school with one discouraging distinction: They’re the most indebted class ever.”

I have often wondered if my choice to go back to school was a good one based on my situation. I was 32 and had no degree to speak of, but I was already deep into a career that required a degree. I was very fortunate to get into IT work during the boom when all you needed was a warm body and some aptitude. (which thanks to my parents getting me a C64 when I was 8, I had in spades) Did I really need to go back to school? Probably not, I took on some debt to do it although because of the program I was able to complete my degree in from 0-BA in two years. In working with a lot of college grads who are now turning to a bleak job market I have to wonder how much longer we will swallow the bitter pill of college.

There are some careers are always going to need a degree, but it seems like apprentice programs and boot camps would serve many people better in the log run. If you are going to take out a small mortgage for a career that pays $30,000 a year it isn’t a good investment or good stewardship of your money. I hope things turn around before my girls are old enough to face this ever growing mountain of debt.

HT to: http://ift.tt/UVpGPS

When Does Saving Turn into Hoarding?

Over at Christianpf.com they had a good discussion on this topic with some good practical ideas on what to look at. I have a question as a thought experiment. Should Christians have a self imposed (I believe any sort of forced cap would be immoral) income or networth cap? I read about a church that did this for their leadership about 15 years ago. It felt like an over reaction to the prosperity “gospel” of the day and I wasn’t sure how I felt about it. But now I wonder if there is some wisdom in it.

We talk a lot here about how personal finance is personal and much of it deals with a position of the heart, but while we can talk about shades of gray eventually grey becomes black and I have been thinking a lot about where grey becomes black in the case of savings v. hoarding.

The Bible clearly states that saving is a good thing (see Proverbs 21:20) and that hoarding is not (see Luke 12:20-21). But is there a clear distinction between the two? And how can we know if we have crossed the line? There must be a line, but is it completely subjective or not? Should we think nationally where we may be in the bottom 10% or globally where if you are American you are in the top 1% no matter how poor you are?

I would love to have a constructive conversation about this because I process by talking things through. Does the Bible speak to this? I think John did in Luke 3 when he tells the people give one of their coats away if they have 2 and their neighbor has none. My family has more coats than we can fit in our closet! But so do most of our “poorer” neighbors.

So, what would this look like? I have no idea as I said it is a thought experiment and I would love to hear from anyone even if you think I am crazy. Drop a line in the comments below.

Survivor Checklist with Lastpass

One big danger in the life of the person who takes care of the finances is death. Ok, sure we could all die, but if I died right now my wife would struggle to know how to access our insurance policies, bank accounts and other financial information. I run a lot of the day to day stuff in our home. While my wife is well informed of our current financial situation there are a lot of accounts out there. It would be a struggle for her to find them all. For years we have talked about a survivor checklist, but have never gotten around to creating a manual one, and I would never update it for each password. Then I thought about a tool I have used for years; Lastpass.

What is LastPass?

If you don’t know about Lastpass it is an amazing password management tool. It securely holds all of your internet account passwords and can autofill them for you. It also generates passwords for you, runs security scans and helps to keep your online account information safe. It can be used as a browser plugin or a phone application (premium service only) It also allows you to keep secure notes, a feature I never thought very much about until I was thinking about this survivor checklist. This is a way for me to communicate all of my passwords to my wife and help her remember all of the things that will need done. (hopefully someone else will be doing it for her).

I created a folder called “In the event of my death” with a note of the same name. It lists emails for our attorney and insurance agents so she won’t need to search. It also has a last goodbye and a few other personal items. These accounts are always up to date because they are what I use every day to access everything.

No one wants to think about death, especially their own. But, we will all die. If you are the person in your family who does most of the book keeping and money management and you don’t prepare something for your spouse to help them in the transition it will only make this time harder for them.

What to include in your Survivor Checklist

- Bank names, accounts and usernames and passwords

- Lawyer’s name and information for your will. (You do have a will, right?)

- Name and Number for Insurance agent for life insurance. (You do have insurance, right?)

- People to be notified of your passing with contact information.

- Any wishes not included in your will

- Perhaps, write your own obituary, that was really hard for us when my dad died.

- You may want to include something like this checklist from the Dennett, Craig and Pate funeral home.

- Copies of your social security, passport, birth certificate, all encrypted with Lastpass

Honestly, this is a lot of work. I would rather not do it, but I love my wife and want to make her life as easy as possible in the event of my passing. That thought helped me get through the process.

Resources:

Life hacker Master information kit.

Considering Stewardship is a site dedicated to managing your time, money, and talent in light of the Gospel.

Edited for broken link.

Giving Differently

Thought like this should make us think about how we help the poor in our context. There is evidence that giving cash directly to the poor may do more for them than expensive programs meant to do for them what we feel they can’t do for themselves. What are your thoughts?

Acts 4:32 – All things in Common

So, I haven’t been posting recently because of a few things popping up at church. I taught a class in February and then I was asked to preach. So, I decided to post my sermon. It is my first time preaching in 8-10 years so I was a little rusty but I hope it blesses you.

Podcast: Play in new window | Download

Things I learned from changing jobs

Changing Jobs

Almost a year ago I went through the process of changing jobs. In that change, I left a nationally known company where I had worked for eight years for a company I had never heard of until the recruiter called. The process I went through to decide if the new offer was better than my current job was pretty thorough. I am the kind of geek that created a spreadsheet comparing everything I could think of: salary, vacation plans, 401(k), bonus opportunities, commute times, holidays and a few other things. I tried to quantify things that were never meant to be quantified. I learned a few things about my self through that process.

I don’t trust God nearly as much as I thought I did.

I actually ended up having two job offers on the table at the same time. (Yes, I know, it is an embarrassment of riches) But, I don’t think I prayed about my new position as much as I should have. I felt that I could quantify everything and it would basically be a mathematical decision. Of course, it doesn’t work that way. But, I am really the kind of guy that doesn’t like to pray about the simple things. “Why bother God with things I can work out out on my own?”

I am still lead by my wallet far more than I want to be.

The fact that I made the decision by calculating the most minute details about money says a lot about how I view money in my life. The major deciding factor on if I took a new job was the money. Granted being a good steward of my skills means I should consider how much those skills are worth and find ways to use those skills to care for my family. But I don’t feel like I should be making decisions based predominately on my wallet, however, I still find security in my bank account and a steady paycheck.

There is Grace for it all

As many mistakes as I made along the way God’s grace is more than sufficient. That is the most important lesson.

All in all I am persuaded that I made the right decision. I am more satisfied with my new job than I was at my old job and I am making more money now. (Funny though, it still doesn’t feel like enough, even though I swore it would be; Ecc 5:10)

image by jakecaptive

What do I do when I have a church money disagreement?

Unless you are one of those dictator Pastors who always does what they want regardless of wise council or you don’t bother to pay attention, eventually you are going to disagree with something your church is doing in regards to money. Then what? Do you stew in bitterness and harbor resentment towards your leadership? Do you stop giving and hold your money ransom until you get your way? Do you attempt to talk things over with leadership in hopes that they will listen to you and change their erroneous ways?

Probably none of those.

Giving to your local church is not the same as doing business with a restaurant whose political policies do not line up with yours. It is fine to boycott a place because you don’t like what they do with their profits that is your right as an American. But your local church is a place that is supposed to help you grow in the Lord and the leadership of your local church, what ever form it takes, are responsible for shepherding you, and they will answer to the Lord for how they do that. We can all be very sinful in our attitudes about money so if you find yourself upset about how your church is dealing with money here are some things to consider.

It is God’s Money to begin with.

The money that God has entrusted to us belongs to him. He has entrusted us as stewards of his many gifts. If God has called you to be a part of your church then he also knows and did know how they would handle his money. That is not to say that church leaders can’t make mistakes, but as I already said they will have to answer to God for their actions as leaders of the church not you. If this disagreement is over something minute then we should consider simply letting it go with prayer for our leaders to gain wisdom or for God to help us see the wisdom in their actions.

This obviously isn’t to say you should be reckless with God’s money but remember that you are part of a larger body and occasionally that means is giving up your right to be right.

They are only human and you can talk to them.

When I did a quick survey of the best pastors I know, to a man, they all said they would want to be addressed directly. Now depending on the size of your church this may be a logistical issue, but you should still try. Those who lead a church are only human and they may very well be in error. However, you should enter the conversation humbly as well. It may be that you are wrong in this matter. If you are a member of the church they should be willing to listen to your concerns and walk you through the situation. Maybe you will help to correct them or maybe they will help correct you. You have to be prepared for both possibilities and humbly pray for God to work on both sides.

Why would you withhold money?

I believe in a free market and the right of a customer to vote with their wallet and do business elsewhere. However, this is not that situation. If you are thinking about withholding your money because of this disagreement and you have already talked with your leadership then you should ask yourself, “Why?” Are you doing this to manipulate your leadership? Are you doing it because you really believe there is a sin issue involved with what the church is doing? The former would not be acceptable while the second one may. I would still seek wise council before making any rash decisions. It isn’t easy when you have a church money disagreement, but it is a great opportunity to grow in grace.

Have you ever been in this type of situation? How did it go? Tell me below in the comments.

Image by imnotquitejack

Create a budget

A budget sounds scary (or boring), but it is just a tool used for making decisions on how to spend your money when your emotions are not running crazy. It is like a map on your journey to financial improvement. If you would like more details on why you need a budget check out this article.

If you haven’t go ahead and read it now. Now, the question is “how do I create a budget?” If you have never actually had a written budget before then figuring out how to create a budget can feel confusing, but it doesn’t have to be.

When I talk with people one on one I usually recommend one or two methods depending on the preference of the individual. I will talk through both here.

Create a budget on Paper.

- Gather up all of your bills for the past month.

- If you don’t have them from last month then keep them when they come this month.

- Track every penny you spend.

- Do it in a notebook, or keep receipts of your spending or use one debit card for all spending then use the statement to actually make your budget you won’t have to guess.

- Put it down on paper.

- If you don’t want to create your own there are plenty of places to find budget templates. However, searching those out may lead to more confusion so here is a simple budget template to get you started.

- Fill in the green spaces that apply to you and the yellow column on the right will tell you what percentage of your income you are spending on any particular category.

- You may not need every single line so only use what suits you. I actually find it most useful to keep categories as broad as possible. But, you need to do what is right for you and knowing that takes experience, so play with it.

- My wife and I have gone through dozens of forms of budgets in our time of trying to organize our finances.

Create a budget with Mint.

- Mint is a free online personal finance program. (Also available on mobile platforms) It is owned by Intuit the same company that owns Quicken and many other programs. They have been in the business for a long time and they are very reputable and secure.

- Sign up for an account on mint.com

- Register your primary spending accounts

- Mint will automatically pull in your all of your account activity and automatically categorize it for you. (Watch out they are not always accurate)

- Use Mints built in budgeting feature to set up the categories for your spending. Mint will let you know how much you have left in every category. You can even set up a alerts to let you know.

Having a budget down on paper, even digital paper is the first step in getting your personal finances under control. There is something about actually writing things down that acts as a commitment device. But, understand that a budget isn’t set in stone. Month to month things may vary and you will have to account for that. For the first few months you should keep a close eye on things and maybe make adjustments as needed. You may have forgotten about something that you will need to adjust for. This is not a “Set it and forget it” kind of thing.

Image by Tax Credits

New Year Goals

New Year Goals

First, let’s talk about why you are taking this course? Why do you want to get your finances under control and pay off debt. Having these reasons straight in your mind can help you succeed when the going gets tough.

These reasons are very important because they will need to be your motivation when things get tough. There will come a time in this journey when you are going to want to give up because things just aren’t fun and exciting anymore. Because things aren’t as easy as you thought they would be or when things aren’t moving as fast as you thought or when you hit a major setback.

Do you want more money when you retire?

Do you want more money when you retire?

Do you want be a better steward of the gifts God has given you?

Do you want to save up for your family?

Do you want to get out from under the crushing weight of debt so you can feel some freedom?

Do you want to get your finances under control

Seek out every reason you can, intellectual, scriptural, emotional and write full sentences about why you want to take this journey. Make these personal reasons that will mean something to you as you move through the process of getting debt under control.

Take your time on this step, it would be easy to cast it aside and just jot down a few things, but the more time you spend on your foundation the better off you will be down the line. You will refer to this down the road when you need motivation.

This is the first in a series designed to help you start the New Year off right. Make sure you don’t miss out on any pieces of the series subscribe to our site by email.

Image by BK