Money as fruit of repentance?

Fruit of Repentance

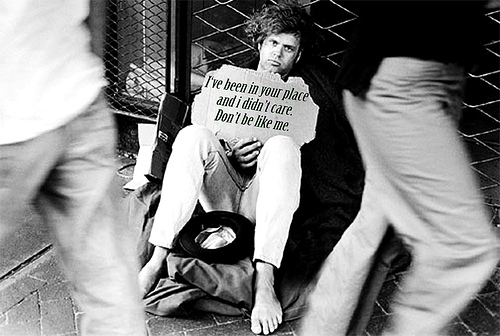

In doing some research for my upcoming book I stumbled into something I can’t believe I had never heard in all my years of being a Christian. It really makes a connection between discipleship and our wallets in a way I had never seen before.

John the baptist calls people to “Bear fruits in keeping with repentance.” They are convicted, or perhaps just scared and ask “What should we do?”

John calls them, not to a generic love, but to a specific material act:

“Whoever has two tunics is to share with him who has none, and whoever has food is to do likewise.”

Tax collectors also came to be baptized and said to him, “Teacher, what shall we do?” And he said to them, “Collect no more than you are authorized to do.” Soldiers also asked him, “And we, what shall we do?” And he said to them, “Do not extort money from anyone by threats or by false accusation, and be content with your wages.” (Luke 3:12-14, ESV)John’s answer to each group was one dealing with money or material possessions.

This has me really wondering, more than I normally do,] about how much of a connection there is between your heart and your wallet. Maybe what Jesus was trying to communicate with us when we said “Where your treasure is there your heart will be also.” is much more serious than we would like to believe.

Jesus challenges us to understand the pull that material wealth and possessions will have on us in this life. If not checked these possessions will pull is hard enough to make us act in ways that are contrary to our profession of faith.

I can remember when our church was moving into a new building and my wife and I had saved up a decent amount of money we intended to use to pay off our second mortgage. When I realized we were going to need a lot of money fast to move into our new building my first thought was pretty selfish:

I need to pay off the mortgage as quickly as possible so I wont have the money to give it to the church.

I know I am the only one who would have thought this way, right? The fact in my heart was in paying off my debt and not in furthering the progress of the Gospel in our city. Is it bad to pay off debt? Absolutely not! But is is bad to be so focused on doing so that you give up being generous? Yes.

How we act with our money is a direct indicator of our much we treasure God and his plan over the things of this world. You always have enough money for the things you love and put first.

How do you think the church needs to work toward showing this fruit of repentance?

Image by ollesvensson

7 Stewardship Principles

There are certain stewardship principles that encompass all other tips we can express. They are not sure fire paths to riches but principles that should guide any Christians view of money.

There are certain stewardship principles that encompass all other tips we can express. They are not sure fire paths to riches but principles that should guide any Christians view of money.

- Be generous first – Deuteronomy 26 calls for a sacrifice of the first fruits of the harvest as a sacrifice. It is a principle of the Bible to give the first to God and not to wait to give your leftovers. You will always have money for what you pay first. People often say they can’t give any money to the Gospel but it is often because they wait until after they have spent it all to think about giving.

- Pay yourself second – Similar to #1 you should pay your self second. If you wait until the end of the month to invest what is left then you will regularly find you have little or nothing left for yourself.

- Have a plan for your money – There is an old cliche that says “Failing to plan is, planing to fail.” I say it this way, “Your money will be spent somehow; you can decide where or let it to chance” You should create a plan on how all of your money is going to be spent. That doesn’t mean just when going to the store, but where you will invest it. Have a plan for all of your money. Call it a budget, or a plan but you have to know where your money is going.

- Don’t leave money on the table – We do it all the time in many ways; here is how to avoid a few of them. Negotiate on everything. You never know when it could save you some money. Make the most of your 401(k), make sure you are getting all the match you can.

- Spend less than you make – This should be obvious to anyone not in government but you can’t survive for long spending more money than you bring in. Eventually those bills will come due.

- Have an emergency fund – Start with a baby fund of $1000 or so, because everything thing that goes wrong seem to cost around $1000. And then move to having 3-6 months of expenses set aside in case you lose your job or have some other financial emergency.

- Understand your insurance needs– Insurance can be an important part of your financial plan. Depending on your situation in life you may need more or less. Insurance can prevent certain financial disasters. A cheaper premium may be cheap for a reason, so research before you do business with any company.

These stewardship principles are crucial to getting off on the right foot. In fact if you were able to stick to all 7 you would be better than 95% of people in America.

image by Dee’lite

Fight the cultural tide

If you are going to try to live a life of simplicity and stewardship you are going to fight the cultural tide all the way. Not only the explicit powers of marketing, which are constantly trying to convince you of some felt need or another, that only they can solve, but there is implicit marketing going on all the time.

If you are going to try to live a life of simplicity and stewardship you are going to fight the cultural tide all the way. Not only the explicit powers of marketing, which are constantly trying to convince you of some felt need or another, that only they can solve, but there is implicit marketing going on all the time.

Think back to how many homes in old sit coms were large enough to have two staircases. We grew up seeing people, even “middle-class” ones, living in luxury that most of us will never see. According to this article from Bankrate even the “2 Broke Girls” live in an apartment that costs $2000 a month. And Penny from the Big Bang theory is living in a $1500 a month apartment by herself with at least a $100 a week wine habit on the tips from the Cheesecake factory. That simply isn’t possible.

These lifestyles are just not realities for most of us, they aren’t even realities for the characters on TV, but we are told over and over again that this is the lifestyle we should have. If you are being a good steward of your money and giving sacrificially it can be hard to make ends meet let alone live up the lives we see around us constantly. In order to live as God calls us to we must learn as Paul said, “I have learned in whatever situation I am to be content.”

It is all to easy to find ourselves comparing our homes, cars and lifestyle to those around us. What we never see is the numbers underneath or the sacrifices that had to be made to accomplish that lifestyle. When I find myself struggling with wanting to keep up with the Jones’ I just assume they are drowning in debt and have no savings. Even if it isn’t true, it helps to crush my pride. I am not quite at the point where I can just be OK with it, it is part of my pride. I confess it.

Living contentedly means that our lives can be simpler. We can be satisfied in Christ and all he is to us and not have to worry about keeping up with the Jones’. Some times that means living with less and some times it will mean living with more, but always being satisfied with our lives and always giving joyfully. It is easy to think and live this way when you are young and your friends are all broke, but it takes a certain level of confidence to live this way without feeling inferior, as you get older and your contemporaries are moving into larger homes and driving newer cars. But, Christianity will be facing much more of an uphill battle as the common culture in America turns more secular, we should get used to it.

What do you think? Let me know in the comments below.

Follow us in the upper right hand corner of the site to keep up with all that is going on.

Maximize Employer Benefits 5 tricks

If you have a decent job you probably have some benefits you are not taking advantage of or maybe not even aware of. This article will show you 5 ways to maximize employer benefits. There may be many ways you are leaving money on the table by not taking advantage of benefits that you employer is offering.

1. The 401(k) – Maximize it for employer contributions

Maximize employer benefits and get more money

A 401(k) is an employee sponsored retirement account. Many companies match your contributions at one level or another which means you may be leaving money on the table if you are not using this plan. Find out what your company does for a match and at least contribute the maximum amount they match.

For example if your company matches 100% up to 4% of your salary like mine does then you should at least contribute 4% of your salary because you are doubling your money. If the company match is 50% up to 4% you should still contribute 4% because a 50% return on your money is still better than most you will get on the market and more than you are paying on any debt you have, unless you are into Frankie the Shark for some money in which case you should pay him first.

2. FSA – Use it to reduce taxes.

A Flex Spending Account allows you to set aside up to $2500 pre-tax dollars to pay for medical expenses in a given year. That means you subtract up to $2500 from the money you are paying taxes on. Keep in mind you can only roll over $500 dollars of that money the rest is use it or lose it; And the Affordable Care Act eliminated the ability to use an FSA to pay for over the counter products to soak up any extra you would have at the end of the year so be careful.

Think about any prescriptions you have or glasses you may need as well as any co-pay you may have to determine how much you may need and aim low because if you don’t use it all it goes back to your employer.

3. Dependent Care Spending Accounts – Reduce more taxes.

These accounts are very similar to the FSA but The dependent care account reimburses dependent day care expenses necessary while you (and your spouse, if you’re married) are attending school on a full-time basis or working. Typically, these would be day care expenses for children, but you can also use this account to reimburse day care for other dependents, such as spouses, parents, or grandparents, who cannot care for themselves. Your dependent must live in your home at least eight hours a day.

There are a lot of technicalities on this one so make sure you understand the detail of how it works. For example I put money into pay for preschool but could not pay for the whole year (as I thought) because the period spanned over two calendar years and I was only able to pay for the calendar year I was in.

4. Tuition Reimbursement – Why not get paid to go to school

Many companies offer tuition reimbursement of some kind if you wish to get a degree or further your education. Many require it to be in the field you are working in and some require you to work for the company for a number of years after you last take the reimbursement but you can often pay the money back.

5. Professional Development – Get paid to get better at what you do.

Many professional companies have training budgets. Our managers tell us that it often goes unused because no one takes advantage of it. If your field offers certifications the company may pay for the training or it may pay for the testing required for the certification.

There may be other ways you can maximize employer benefits; it it all depends on what your company has to offer. Take a look and ask around. Often there are benefits that are almost secrets in companies.

Betterment Review

I have been using Betterment since February of 2012 for my long term investment and savings. I have wanted to do a Betterment review for a while but wanted to break it in before I gave my opinion. Betterment is a website that makes investing simple enough for everyone. It makes investing stress free and easy. I have tried picking my own stocks but fees ate up whatever profit I may have gained. Betterment’s fees are incredibly low and they allow you to set a risk level you are comfortable with for all you different savings goals.

Getting Started

If you are trying to save money you know now is a bad time. Low interest rates are great if you are looking to buy a house but if you want to save your money low interest rates are not your friend. Unless you have 50,000 or more to invest a lot of firms won’t even talk to you. This is one of the reasons I love betterment.

Betterment breaks down your accounts by the goal you are looking to achieve. So, when you create a new account it will ask you to select a goal. Like Safety Net, IRA, Educational.

Then you simply answer a few questions about your goal. How much would you like to have in that goal at what time? Do you need 20K in 10 years for a child’s education? How much can you start with? Based on those questions Betterment will recommend a portfolio on a simple Stocks(Risky but rewarding) v. Bonds (More secure but less reward) scale. So, for our down payment goal which we hope to use in the next few years we are less risky and have 80% in bonds but in our daughters college accounts which won’t be needed for 10 years at least we use 80% stocks. It will also tell you how much you need to deposit each month to reach your goal and that can be automatically done through Betterment as well and automatically drafted from your selected checking account.

Customer service was remarkable when I called Betterment to see why I couldn’t have more than three goals. (This was early on the now allow many more) I got a real person almost right away who was very helpful and got me into the beta test for more goals.

Returns

So far the best thing about Betterment besides the automation, which I am a big fan of has been the returns. Keeping in mind that past performance does not indicate future performance and all that we have had some great returns for our the college funds. The total balance has some more conservative accounts like our house down payment account but over all I have been very please with the returns. The functionality of the site is superb making it very easy to get started saving with more than .25% interest rate or whatever banks offer these days. They even let you try it out for 30 days free.

Our overall rate of return has been 8.7% but our college funds are over 17%.

Fees

The fees are simple and inexpensive as well.

- If you deposit less than $100 per month it is a flat $3

- If you auto deposit at least 100$ a month your fee is a flat .35%

$5000 = $1/month - If you have $10000 or more across all of your goals your fee goes down to .25%

$10000 = $2/month. - Over $100,000 in all of your goals and your fee is only .15% and you get many other options to customize your plan.

Over all if you are ready to make the move into having your money make money for your Betterment is a great way to get started.

This article contains affiliate links… You get $25 and I get $10 if you sign up through these links…Betterment

Please give me my idol

Am I asking God to give me my idol?

Image by itineranttightwad

I have been seeking a new job recently and have had some very promising leads. I am hoping to have a decent pay raise when I take a new position and I have found myself thinking about all the things I will be able to do with this new money; how much better it will make my life; how much safer and more secure I will be. All things I should be relying on God for, not a job.

It is amazing how easily these little bits of sinfulness can slip into our lives; it is no wonder that Martin Luther called the human heart an idol factory and why Jesus said it is hard for a rich man to enter the kingdom of Heaven. It is hard for us who have so much to realize how much we need to rely on God for our daily bread.

We Americans, even the poorest of us are in the among the richest in people in the world and because we don’t want for many necessities we don’t think daily about how desperate we are and how much we cannot do ourselves.

Personally, I was looking for this job to be my functional savior against my lack of satisfaction. I am not satisfied in my God and those wonderful things he has given me. Sure, I say how much I am thankful every night when I pray over our meal or with my daughters before bed but the words have a hard time sinking in to my stony heart.

I often talk about the story of the rich young ruler from Matthew 19.

And behold, a man came up to him, saying, “Teacher, what good deed must I do to have eternal life?” And he said to him, “Why do you ask me about what is good? There is only one who is good. If you would enter life, keep the commandments.” He said to him, “Which ones?” And Jesus said, “You shall not murder, You shall not commit adultery, You shall not steal, You shall not bear false witness, Honor your father and mother, and, You shall love your neighbor as yourself.” The young man said to him, “All these I have kept. What do I still lack?” Jesus said to him, “If you would be perfect, go, sell what you possess and give to the poor, and you will have treasure in heaven; and come, follow me.” When the young man heard this he went away sorrowful, for he had great possessions.

And Jesus said to his disciples, “Truly, I say to you, only with difficulty will a rich person enter the kingdom of heaven. Again I tell you, it is easier for a camel to go through the eye of a needle than for a rich person to enter the kingdom of God.” When the disciples heard this, they were greatly astonished, saying, “Who then can be saved?” But Jesus looked at them and said, “With man this is impossible, but with God all things are possible.” (Matthew 19:16-26, ESV)

We are so attached to our possessions that although we would deny it with our words our hearts are very much like this rich man. Jesus is pointing out the idol that sat at the altar of this young mans heart and he refused to cast it down. What I find interesting is that the disciples were astonished that it was hard for a rich man to enter the kingdom of heaven. How often to we assume that material success is a sign of God’s approval? I have heard it when it comes to money and the individual. “God is blessing me with this new car because of my obedience” Applied to churches “They must be doing something right because they have a huge crowd”

Jesus makes it pretty clear here and other places that external circumstances are not a direct indication of God’s approval or disapproval. ” For he makes his sun rise on the evil and on the good, and sends rain on the just and on the unjust.” (Matt 5:45)

This story serves as an example to me and hopefully to us all that our things are never to be more important to us than our Lord. It is not our jobs or our family that ultimately provides they are conduits through which God provides our needs.

Image by itineranttightwad

What is a 401(k)?

What is a 401(k)?

Photo by 401k 2013

As I have written previously I work with a lot of college students in our church as a part of my ministry there. There are always questions about 401(k)s; What they are how they work. The fact is that many people simply don’t understand this very important retirement vehicle.

So, what is a 401(k)? It is a savings plan named after the section of the law that created it. It allows an employee to take a portion of their pre-tax income, up to $17,500 for 2013,(Those over 50 are allowed to add $5,500 to that amount) to a qualified employer sponsored investment plan. Many employers choose to match their employees contributions to some degree adding additional money to the pot.

So, what do those things mean? Pre-tax dollars means that the money contributed to your 401k are not counted as income when you are taxed. If your paycheck was $1000 and you contribute $100 to your 401k then you only pay taxes on $900. ($1000-$100) This allows you to save money up front on taxes. Because you will pay taxes on the money when you retire it is called a tax deferred plan. This also begs the question “Will taxes be higher now or when I retire” I would guess taxes have no where to go but up since we are only paying for 2/3 of the government we have now and we will eventually have to pay for the remainder.

Employer match

This is one of the sexiest aspects of the 401k plan. With the average 401k plan employers contributed 4% of the employee’s salary most commonly in the form of a direct match. An employer will match dollar for dollar every dollar an employee contributes up to a certain percent, the average is 4%. Meaning that if Joe contributes 4% of his paycheck to his 401k the company contributes the same amount to his 401k. This work out to be a 100% return on investment; Joe doubles the money in his 401k.

Not all employers do a direct percentage match some match $.50 on the dollar or some other amount but knowing how your 401k plan works is important to making the most of your plan. As in our above example Joe’s employer matches up to 4% of his salary. This means that if Joe is contributing less than 4% to his own retirement then he leaving his employers money on the table.

Getting your money out of your 401(k)

Getting your money out of a 401(k) can be difficult or have penalties depending on the circumstances of your plan. Traditionally, you can only make withdraws from a 401(k) under certain circumstances.

- When the employee retires, becomes disabled or is no longer employed by the employer who sponsored the plan.

- The employee hits age 59.5

- The employee experiences a hardship as defined under the plan, if the plan permits hardship withdrawals

- Upon the termination of the plan

With some plans it is possible to take a loan of 50% of the vested value of the account but not all plans allow for this option.

Summary

A 401(k) is a retirement plan that has some great aspects and that also has some drawbacks.

Pros:

- Most employers contribute additional money to the retirement of the employee.

- Tax benefits.

Cons:

- Mandatory withdraws at age 70.5

- Taxes are likely to be higher when you actually have to pay them on the money in the account unless you believe you will be in a lower tax bracket when you are pulling money from your account.

Obviously, I can’t cover everything there is about 401(k)s but hopefully this gives a basic idea about what they are and how they are used.

Photo by 401k 2013

Give to everyone? Is Jesus Kidding?

Image by jorgempf

Are we really called to give to everyone? Luke 6:30 and Matthew 5:42 are two scriptures I would really like to remove from the Bible, if I am being honest.

Give to everyone who begs from you, and from one who takes away your goods do not demand them back.

I live in a city and people are begging all the time, on every freeway off ramp, on every street corner. I have been approached multiple times in parking lots with stories of running out of gas and loss of debit card, and a dead cell phone. How am I to handle these things as a Christian? These scriptures make it fairly clear that I am to give to anyone who begs (some bibles say “asks”), but Paul says that anyone who doesn’t work doesn’t eat. So, it is not as straightforward as just giving to everyone, at least I don’t want it to be.

I want to handle my money responsibly, but I also want to be obedient to Jesus and not be selfish with my money. How do we handle this dilemma. I will be upfront that I don’t know if I have a solid correct answer. This article is more about exploring the issue. If you are looking for a hard and fast answer: move along.

Why do we not want to give to everyone?

As with many things, asking why we feel a certain way can be very helpful.

- I don’t like the idea I’m being ripped off.

- I don’t want to be made a fool of.

- I don’t want to be parted with my hard earned cash under false pretenses.

I give all the time when people I know are in need because I know them and their situation. They aren’t faking it.

The gospel answers to these questions, of course, come from a proper understanding of stewardship; It isn’t my money in the first place, it is God’s. He has the right to require it of me anyway he likes, if I am to call myself a believer. Does it matter if the individual is sinning by lying to me. That is up to God to handle and he will either by forgiving them and making them his children or by allowing them to bear the punishment for their sins.

So, am I simply worried about being a bad steward of God’s money? Maybe, but them I am reminded of a story I have heard about CS Lewis.

One day, Lewis and a friend were walking down the street and came upon a begger who reached out to them for help. While his friend kept walking, Lewis stopped and proceeded to empty his wallet. When they resumed their journey, his friend asked, “What are you doing giving him your money like that? Don’t you know he’s just going to squander all that on ale (beer)?” Lewis paused and replied, “That’s all I was going to do with it.”

If I am honest, even if I gave $20 to everyone beggar on every off ramp holding a sign that says “stranded” I would still give away less money than I waste on frivolous things.

Is there a biblical reason not to give to everyone?

Money is at best a temporary solution to the issue facing the person asking. Giving money to a person on the street is a great way for us to feel better about ourselves without actually doing any good for the person we give the money to in many cases. It seems to me that in the biblical context people knew more about one another. If you saw the same person begging in the same place every day for a year you could assume they were not able to work. You could ask if you didn’t already know their story. However, in our day that is very unlikely.

Paul was pretty clear in saying that if a man doesn’t work he doesn’t eat. Laziness was not acceptable. But how do we know if that is the case if we don’t have a relationship with the people in need?

As Christians we are called to give and help above and beyond. That is why Jesus called us to give to everyone who asks. He didn’t qualify it because he knew we would look for any excuse at all to not obey.

What do you think? What are your considerations when it comes to giving to everyone that asks of you?

Teaching kids about money

Teaching Kids About Money is not a New Law

Teaching Kids About Money is not a New Law

Teaching kids about money through a gospel lens is is something I am still working on figuring out. Our daughters 7 and 5 are still learning how to count money let alone spend it. However, I want them to understand early how money plays a role in our life. I want them to see Christ as sufficient and to not think money will fulfill their life. It shouldn’t be that hard right?

But, as I researched some articles to write this I discovered something. Most of the articles I found from big time Christian resources were no different the advice you would read from secular sources: Teach them to save early, teach them how interest works against you, make them earn their money so they understand the value of it and show them how to spend it properly. The only thing that set them apart from secular resources was talk of the tithe.

In their book Give Them Grace: Dazzling Your Kids with the Love of Jesus Elyse Fitzpatrick and Jessica Thompson say, and I am paraphrasing because for the life of me I can’t find the quote, “If your parenting isn’t any different than a Jew, Muslim or a moral humanist you are not parenting as a Christian.” We can have all the steps and rules we want when it comes to our money and we will only create little pharisees. Our parenting, in every way, should always call us back to the cross and the gospel of Jesus Christ.

Honestly, I started to write this article as a to-do list just like the ones I read.. That is why I was so irritated by what I found when doing my research. There are already tons of those articles out there here are a couple:

Teaching Kids about Money – We can’t assume the Gospel.

But, like so many of our sermons these articles assume the gospel instead of preaching it. The gospel calls us to give as we have been freely given. I believe the gospel calls us not to be selfish with out money. The Gospel calls us to give what we have cheerfully and sacrificially. The Gospel calls us to make Jesus the center of our life and live like he is completely sufficient. The question is how to do instill those principles in our children when we are living like it isn’t true. We work hard to get more to keep up with our neighbors and perhaps to give more but only to “sanctify the rest” so we can feel good about spending it however WE want.

Even by following a list of to-do’s, like the ones above, we need to be careful that we are not teaching our children to rely solely on their own wisdom to provide for all their needs, lest when financial trouble befall them they blame God because they feel like they followed all “His rules” and it didn’t work. Then God becomes a liar in their eyes because they equate good financial advice with the gospel.

Those of us who sinfully find our security in money love to look at the book of Acts and brush off the “socialist” lifestyle they lived as being simply a description of how they lived and not instructional as to how Christians are to live. However, giving statistics of Christians bear out that we have a lot to learn from those in the early church.

Maybe I will write a list of ideas on the practical side later because I do believe there is a need for that , right now I feel like the church needs to turn its eyes back on the cross when it comes to money. I know I do.

Where is your missing money?

Image by Ano Lobb

We all have missing money. You get to the end of your week and you know you had enough money to pay for everything you needed, but somehow you are coming up short. Where is your missing money?

Look, I have been talking, writing and lecturing about personal finance for years now and it still happens to me. I know exactly how much extra money I have in my various accounts. I know that we deposit extra into our main bank account to ensure we don’t overdraft. I know we have extra paychecks a few times a year so I know there is technically extra in the account we pay our bills from. So, I spend it because I know it is there. That is where my missing money is; living it up outside of my budget.

My guess is you have a few dollars floating around outside your budget. We all do. This problem arises when you allow money to sit idly in an account somewhere doing nothing. It will run away from you when you aren’t paying attention. Money wants to be spent, or used in some way and it will find a way to get what it wants. What can you do to keep your hard earned dollars from becoming missing money? I am glad you asked.

Give your money something to do.

The secret to keep your money from going missing is to give it something to do. You money, like most of us, wants to feel like it has a purpose. You need a plan for all of your money, give it something to do. It doesn’t matter if it is paying off debt, paying for your bills, or being put in a nice quiet interest bearing account or investment to make more money for you.

Alright, the metaphor has gone far enough. I recommend you automate everything with your bank to make sure all of your money is going somewhere and doing something. Here are a few ideas.

- Recurring bills that are the same each month. (mortgage, car loan, insurance etc…) — Have an account where money goes to pay these bills that you can’t spend from. Each month set up an automatic payment with your bank to pay these bills’ total balance each month.

- Recurring bills that are not the same every month (utilities) — Call each of your utilities and see if you can make them stable. Many utilities will let you pay the yearly average of your bills all year. That way you know exactly how much you are going to pay each month.

- Any money left in your budget — Use it to pay off your debt if that is your goal, or put it in an interest bearing or investment account so you can’t spend it. That way it isn’t in a place where you can spend it on frivolous things.

Following these types of ideas will keep you from asking “Where did my money go?” It just won’t be available to spend.

What other ideas do you have? Tell us in the comments.