My extra income adventure: A New Series

I am going to be kicking off a new series on this blog. I have been interested in producing some extra income in my life in order to help to pay for the down payment for my house. I have often looked into passive income ideas and it seems like most of them are anything but passive. Passive income is income that you don’t directly trade time and labor for money. Examples would be royalties, or licensing etc. Although my book would fall under this category I don’t have any delusions about making millions of dollars from it. (although it would be nice)

I am going to be kicking off a new series on this blog. I have been interested in producing some extra income in my life in order to help to pay for the down payment for my house. I have often looked into passive income ideas and it seems like most of them are anything but passive. Passive income is income that you don’t directly trade time and labor for money. Examples would be royalties, or licensing etc. Although my book would fall under this category I don’t have any delusions about making millions of dollars from it. (although it would be nice)

I had considered getting a second job, but didn’t want to give up time with my children who I only see 3 hours a night as it is. So, one of my qualifications for these ideas is that I am not simply trading my time for money directly. (I will do this job for x dollars) I hope to find other ways to work once and make money over and over with that work. I plan on doing some of this by outsourcing some of the work that I can’t do, or don’t have time to do. If I do my calculations correctly the Virtual Assistant (VA) should pay for themselves.

I have some money that I am able to invest in business ideas to capitalize a few of them, which makes me fortunate. If you want to see this done with almost no money check out UpwardsofTwenty. He is starting with $20 dollars and investing in interesting ways to grow from that $20 to where ever he ends up.

My plan is to start with some small ideas that I can put into place once and make more than an hourly wage in the process. I am not going to throw my money at any get rich quick schemes, that would be bad steward ship although even those crack pot ideas have real extra income ideas as their kernel of truth.

After I have completed my first venture I will update you with the plan I followed and the money I made. I plan to be as open and honest as I can with this part in the interest of transparency.

In order to keep myself sane I am going to look at any money invested that loses money as the cost of education. I find that I am very hesitant to take risks but hopefully I can break myself of that mindset with some small victories.

First Ebay Sale

As part of my New Year resolution I have posted my very first Ebay sale. It is a hard drive that has been sitting on a shelf in the box for a while now. The reason for the sale is two fold; we are looking to save up for a down payment for a house and so I am going to try to sell some things we have had around the house that we no longer need and secondly our house feels too crowded with stuff and we are looking to simplify and get rid of things we no longer need or use.

A lot of things have changed since I last looked at selling things on ebay which made my first ebay sale much easier.

- Setting up the listing was incredibly simple – I was able to model my listing after others already in the system and it took care of most of the information for me. I took a few pictures with my phone and up loaded them.

- Shipping was a breeze – I was very conserned with how to deal with shipping. I don’t ship a lot of things and I did a little research with UPS and USPS but turns out ebay has you covered there as well. They knew my product and suggest a flat rate USPS option that I had already concluded I needed. It made me feel much safer.

- Anyone can do a “Buy it Now” – Last time I has looked into it (admittedly a long time ago) only experienced sellers could do a buy it now sale. Meaning you don’t have to play the auction game but could simply buy it outright.

The item sold after a week for $35, which is more than I paid for it. All in all Ebay has improved a great deal since the last time I had looked into selling. It could be a great way to earn some money and simplify your life by getting rid of some things you no longer need.

Extra Income, what should I do?

To Pay or not to Pay (off your debt)

I get a form of this question all the time. Should I pay off debt or invest it? Paying off existing debt is a safe bet. Think of it this way, if you are paying 19% on a credit card then by paying off that card you are saving 19% interest. That is money in your pocket every month that you can use to pay off other bills or start investing.

If you debt is low interest and/or tax deductible you may be better off by paying your monthly minimums and investing the extra money you have. Here is why..

Using debt to make money

Imagine if I told you that I would pay you 100$ tomorrow if you loaned me 90$ today? Suppose that you didn’t have 90$, but you could borrow it from a friend and pay him back 95$ next week. You would make 5$. You can do the same thing with your debt if you have a solid investment plan and some time.

According to most resources, the average return from the stock market over the long term is between 7% and 12%. If you are paying 4% on your mortgage, for example, you could take extra money and pay off that debt or you could take the same extra money and invest it. Sure, you would be paying interest on that money, but over time you will make more money investing. There would be some months where you may not, if the stock market has a bad run, but over time you should make more money.

This type of decision is not to be entered into lightly. Previous performance is no indication of future performance. That means that the stock market could make 1% over the next 30 years and you would lose money.

Additionally, it may be more important for you to be out of debt and play things safe. You may want to leave the rat race and start your own business. This is why I normally tell people to pay off their debt. It is the right emotional choice for most people, but it is possible to make more money and possibly pay off your debt sooner with the proper investment strategy.

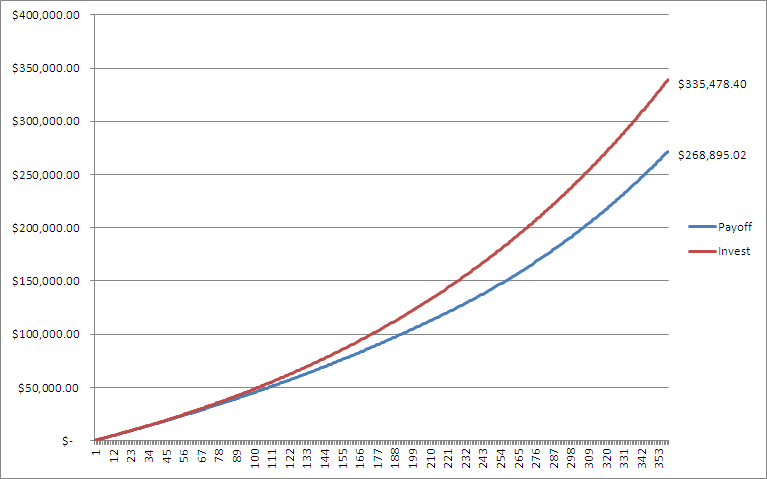

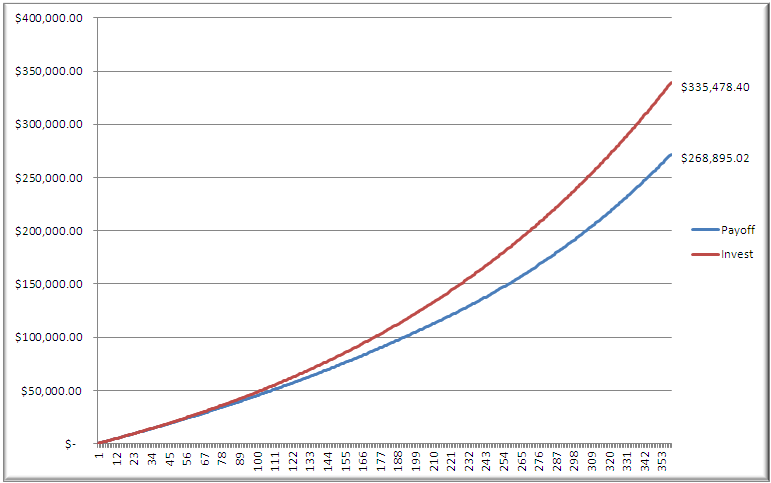

The chart below shows the difference in total value over 30 years when you invest at a conservative 6.5% instead of paying off a mortgage that has a rate of 3.5%. The numbers include the equity in the home as well as investment income. Once the mortgage is paid off the money that was being used to pay off the mortgage is then invested at 6.5%

Of course, there are many assumptions involved in these calculations. Your particular situation may be different, but many people have never even considered the benefits of not paying off their debt.

This is for informational purposes only, everyone should do their own investigation and due diligence.

Give Yourself a Raise

One of the things I like to tell people in my stewardship presentations is that it is possible to give yourself a raise of roughly $2900 a year, depending on your personal situation. Not only is this possible, I highly recommend it to anyone who wants to act responsibly with their money.

Photo by TALUDA

If you are looking to pay off debt, make ends meet, or just invest YOUR money so YOU gain the interest you owe it to yourself and your family to give yourself a raise.

Now for a little background…Every paycheck the government takes a ton of your money before it even hits your pocket and every spring people get really excited that the government makes them fill out paperwork to get back the extra that the government took out in the first place. We call it tax season.

If you get a tax return back every year it means you are giving the government too much money every paycheck and they hold it all year and then give it back to you interest free when you file your taxes.

I don’t want to get political, but I believe it is irresponsible to allow the government to take your money all year only to give it back to you interest free in the spring.

The average tax return in 2011 was $2900. By filling out a new W-4 form you tell the government to take less of your money each paycheck. It reduces your refund but you will have more money in your pocket every paycheck. How do you decide what is right? The IRS actually supplies a handy little calculator for just such an occasion. It will give you the correct number to enter on your W-4 to get you the smallest refund and the largest paycheck. I, personally, like to have just enough money to pay for turbotax but you should do what you are comfortable with. For years before I knew the calculator existed I just moved my W-4 number up a each year so I was paying less every year.

The point is, that is your money they are taking and holding. Imagine going to the grocery store and paying too much for your groceries every week but not getting any change until the end of the year. You wouldn’t be excited about that money at the end of the year! It should have been in your pocket all along. That is exactly what happens with your taxes. People over pay their tax bill and get excited when they get their “change” in one lump sum because they don’t understand the process.

For this to work you must have a regular paycheck which has taxes withheld If you are responsible to pay your own taxes then this won’t work. You must also get a tax refund at the end of the year, if you don’t then you can’t get that money back throughout the year.

If you are looking to get more control over you money, to pay off debt, save for the future or just keep it out of government hands. This is a great first step.

As always you should do you own due diligence when it comes to these issues. This article is for informational purposes only and is not to be considered tax preparation or legal advice.